Author byline as per print journal: Babar Khan, BPharm, MPH, PhD; Brian Godman, BSc, PhD; Ayesha Babar, BPharm, MPhil; Shahzad Hussain, BPharm, MPhil; Sidra Mahmood, PharmD, MSc; Tahir Aqeel, BPharm, MPhil

|

Introduction: There are concerns over the quality of generic medicines in Pakistan. This is due to perceived non-compliance with good manufacturing practice (GMP), whereby the quality of the raw materials is not being assessed. If not addressed, this will impact on the potential for generics exports from Pakistan, as well as on patient care. Consequently, there is a need to assess the current assessment and regulatory situation in Pakistan and to recommend a way forward that ensures the future quality of products. |

Submitted: 7 July 2016; Revised: 8 November 2016; Accepted: 14 November 2016; Published online first: 25 November 2016

The pharmaceutical market in Pakistan was worth approximately US$2.3 billion in 2014 [1]. At present, Pakistan produces a variety of medicines and meets approximately 90% of the demand for domestic finished products. However, currently Pakistan only produces a limited amount of the active pharmaceutical ingredients (APIs) needed for medicines consumed in Pakistan [2], with more than 90% of raw materials/APIs coming from China and India.

There are concerns over the quality of medicines manufactured in Pakistan due to perceived non-compliance with good manufacturing practice (GMP) requirements outlined by pharmaceutical manufacturers [3]. These include checks on the quality of APIs being used to produce oral tablets [3]. GMP requirements are included in the Drug (Licensing, Registering and Advertising) Rules (Schedule-B II), which were enacted in Pakistan in 1976 [4]. However, since then, GMP and other registration requirements have not been updated [5]. This means that there have been no updates or revisions following the creation of international standards or World Health Organization (WHO) guidelines [6]. With over 1,200 registered medicines and over 80,000 registered drug products in Pakistan [5], coupled with physician concerns over the safety and efficacy of lower cost generics, the country sees high levels of prescribing of originator products [5, 7, 8]. This is a public health concern as self-pay for medicines in Pakistan is widespread [9] and therefore there are implications for affordability and subsequent adherence rates, especially for treatment of chronic diseases affecting the lower paid [10–12]. Patient care is not compromised with generic medicines that meet agreed quality standards, including bioequivalence levels, across a wide range of disease areas [13–19]. Concerns over generic immunosuppressants are also reducing [20].

There is inconsistency between the information to be included in application dossiers required for authorizing a medicine in Pakistan by the Drugs (Licensing, Registering and Advertising) Rules, 1976, and those stated in the Drug Regulatory Authority of Pakistan (DRAP) Act, 2012 [21]. In this Act, Schedule-I states that the pharmaceutical dossier should include a set of the following documents for submission that give all information on the technical aspects of a product’s manufacture:

a. Master formula

b. All ingredients both active pharmaceutical ingredients and inactive excipients added with their safety profile data

c. Complete manufacturing procedure of the drug, biological or medical device

d. Quality control steps and procedures at each level of raw material selection, in-process testing, finished drug testing and stability testing

e. Clinical trial data and published reports about the safety and efficacy of the drug

f. Complete details of manufacturing plant and equipment, quality control laboratories and equipment

g. Warehouse capacities and facilities; details of human resources available and the latest cGMP (current good manufacturing practice) report shall also be part of this document set

h. Any other information required by the Registration Board for establishing the safety, efficacy, bioavailability, bioequivalence, or biosimilarity of the drug.

Section 7 (c) (ix) of the DRAP Act, also emphasizes the systematic implementation of the International Council for Harmonisation of Technical Requirements for Pharmaceuticals for Human Use (ICH), WHO and US Food and Drug Administration (FDA) guidelines [3, 6, 22]. All of these guidelines suggest that application for the registration of medicines in a country should follow an internationally harmonized format known as the Common Technical Document (CTD). The CTD consists of five modules [23]:

However, despite many developing countries implementing such standards, these standards are not implemented in Pakistan. The lack of implementing such standards demonstrates the continued weaknesses of this registration process [5].

The quality of medicines in Pakistan is of major concern. DRAP is currently unable to effectively check the quality of all APIs and finished products through the available surveillance testing laboratories that are under governmental control. These materials are typically only tested to be quantified, and not for the identification of impurities, nor do they undergo any other pharmacopoeia tests. In addition, most of the laboratories involved in conducting these tests appear to contain out-dated instruments and materials, and there are concerns over levels of staff training and availability, as only a limited number of staff have been hired in recent years. This is despite such regulations being included in current laws [24].

The medicine registration process in any country is key to the availability of medicines that meet agreed quality targets. Concerns over the quality of generics produced in Pakistan is currently resulting in low exports [25] and impacting on patient care, especially for patients with chronic diseases.

There are also concerns that the basic and semi-basic industry involved in the manufacture of raw materials in Pakistan has not flourished due to unfavourable policies towards the protection or security of businesses. This is reflected by the fact that only 33 manufacturing units are currently involved in basic or semi-basic manufacturing of pharmaceuticals in Pakistan [26]. This compares with approximately 600 active licensed manufacturers of finished products in Pakistan [27]. In addition, among these 33, only seven manufacturing units currently appear active further demonstrating problems with current policies [26].

Considering these concerns, this study has assessed the quality of APIs in Pakistan and seeks to use the findings as a starting point for suggesting improvements in the registration process for oral generic tablets. We chose ibuprofen for our study in view of the extent to which it is prescribed in Pakistan, which is 12% by value of the analgesic market. The analgesic market currently has a growth of 20% per annum [28]. In addition, APIs of ibuprofen are produced both locally and imported. For ibuprofen, there are specific concerns relating to potential impurities in the light of pharmacopoeia specifications. The findings will subsequently serve as a guide to suggest improvements for the pharmaceutical drug registration process in Pakistan, to ensure good quality, safe, effective and affordable medicines are being produced that will help improve patient care in Pakistan, and potentially boost exports.

Collection of ibuprofen API samples

Twenty-seven samples of ibuprofen APIs used by manufacturers in Pakistan were obtained, together with their Certificate of Analysis (CoA). The CoA contained details regarding the results of tests and their values and limits (including assay values) of relevant batches, as well as information about the manufacturer. The US Pharmacopeia (USP) reference standard ibuprofen was obtained from Abbott Laboratories, Pakistan (originator manufacturer of ibuprofen). Coding was undertaken on all collected samples, with all samples stored in closed containers. Desiccators were used to avoid moisture absorption.

Quality assessment

The quality assessment of the ibuprofen samples was performed using the following methods:

1. Identification test

All samples were identified using the following two methods:

For all API samples and the USP Reference Standard (Abbott Laboratories, Pakistan), the solutions were prepared in 0.1 N Sodium Hydroxide with a concentration of 0.025 g per 100 mL, equivalent to 250 μg per mL of ibuprofen. Respective absorptivities at 264 nm and 273 nm on the anhydrous basis were noted.

For the UV-Spectrophotometer limits, the absorptivities were calculated on an anhydrous basis, and should not differ by more than 3.0% at 264 nm and 273 nm, as per USP limits.

The testing of ibuprofen against USP specifications was undertaken in one of Pakistan’s ‘Appellate Laboratory’, known to perform to the highest standards. The utilization of an USP approved laboratory to undertake the testing has significance in terms of the reliability of the results, negating the need to test the samples in other USP international laboratories in either Brazil or China or India.

2. Assay test

USP specifications mention the following limits for assay testing, ‘Ibuprofen (Active Pharmaceutical Ingredient) contains not less than 97.0 per cent and not more than 103.0 per cent of C13H18O2, calculated on the anhydrous basis’ [29]. The USP only documents one related or impurity substance, this is in contrary to the British Pharmacopoeia specifications where 18 substances are mentioned. However, the identification and characterization of related or impurity substances is out of the scope of this paper.

The Assay Test procedure

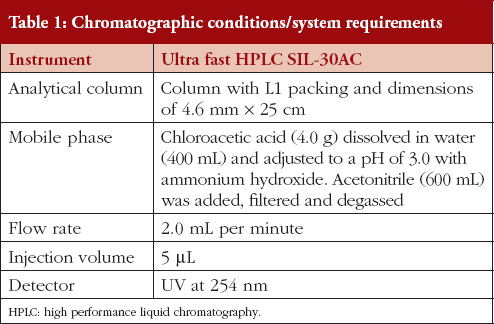

Mobile phase

Chloroacetic acid (4.0 g) was dissolved in water (400 mL) and then adjusted to a pH of 3.0 with ammonium hydroxide. Acetonitrile (600 mL) was added, then filtered, and degassed. Amendment or modifications were done as per the requirements of System Suitability.

Preparation of standard solution

A solution with concentration of about 12 mg per mL was prepared by dissolving USP Ibuprofen RS (accurately weighed) in Internal Standard Solution.

Assay preparation

1200 mg of ibuprofen, accurately weighed, was transferred to a 100 mL volumetric flask, diluted with Internal Standard Solution to volume, and mixed. Table 1 contains details of the chromatographic conditions.

The L1 column packing used was Octadecysilane C18 as C18 is generally more retentive than C8.

Test for system suitability

The peak response was recorded after repeated injections of five to six consecutive standard solutions before injecting the sample solutions. This was repeated after completion of work, to observe the consistency of performance of the system.

Acceptability criteria

The qualification criteria for the system suitability test was that there should be less than 2% Relative Standard Deviation (RSD) for five replicate injections of the standard solution, with not more than 2.5 tailing factors for the individual peaks.

Procedure

Equal volumes (approximately 5 μL) of the Standard preparation and the Assay preparation were separately injected into the chromatograph. Chromatograms were recorded and the response for the major peaks was measured.

The quantity of ibuprofen in mg was calculated using the formula: 100 C (RU/RS) where:

1. Identification test

Through FTIR (Fourier Transform Infrared) Spectroscopy:

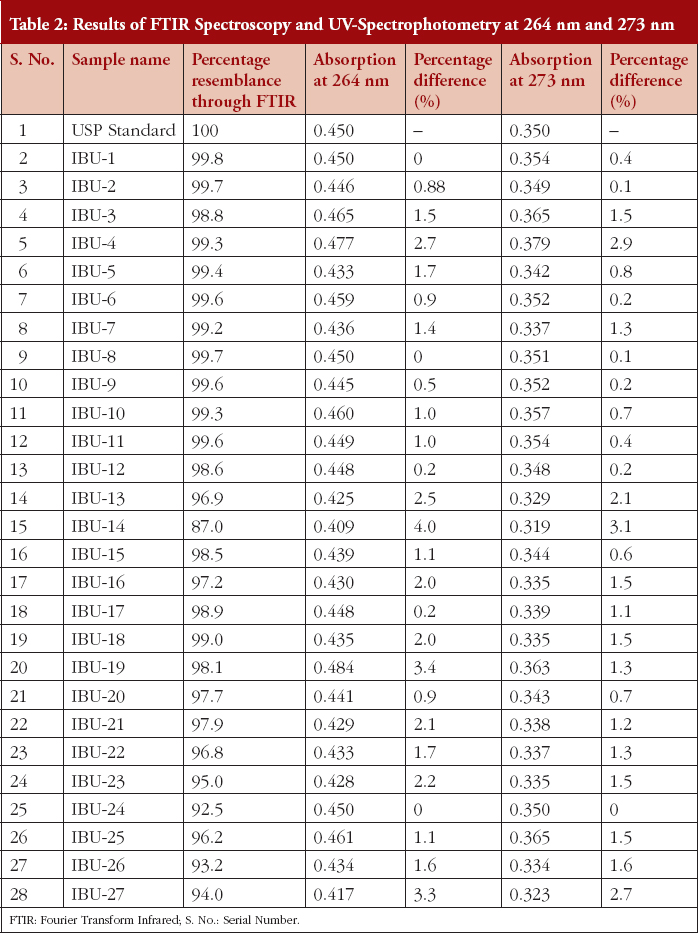

Table 2 documents the percentage resemblance of the FTIR spectra of the 27 samples, to the USP standard spectrum. It also shows the percentage difference between the 27 samples and the USP standard spectrum, for the 264 nm and 273 nm peaks, recorded via UV-Spectrophotometry.

For measurements taken on the same day, precision ranged from 0.23% to 0.62%, and accuracy ranged from 99.6% to 100.3%. For measurements taken on different days, precision ranged from 0.24% to 0.52%.

2. Assay values

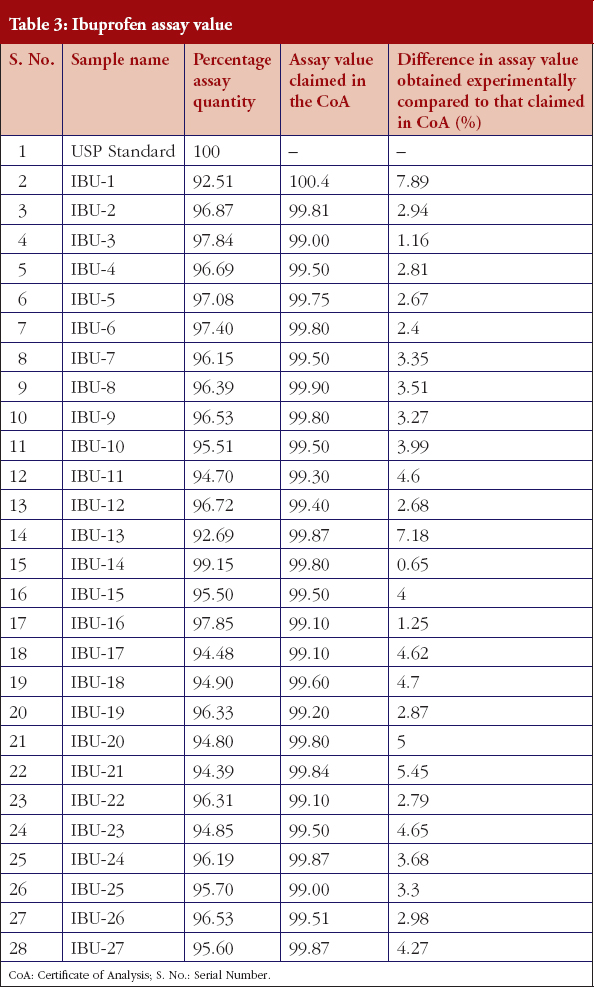

Table 3 documents the assay values of the 27 samples and the ibuprofen USP reference standard.

The results reveal both positive and concerning aspects surrounding the APIs currently used in the production of generic ibuprofen tablets in Pakistan.

All samples, except sample IBU-14, passed the Identification test through FTIR and UV methods as per the requirements of USP specifications, see Table 2. Using the analytical methodology or assessment suggests that 96% API samples passed the test and can be approved and marketed as ibuprofen.

However, 22 out of 27 (81.5%) of the ibuprofen samples failed to comply with the USP assay limits, i.e. 97% to 103%. Interestingly, sample IBU-14 passed this test with highest percentage of assay value, i.e. 99.15%, see Table 3. IBU-14 also showed minimal difference in assay value to the values mentioned in the product CoA, see Table 3.

Secondly, one extra peak was noticed in the chromatograms of six (18.5%) of the samples, i.e. IBU-3, IBU-4, IBU-5, IBU-10, IBU-19 and IBU-25, at approximately the same time, i.e. between 3.1 to 3.3 minutes.

Thirdly, the comparison of assay values obtained using our methodology, versus those claimed by the manufacturer in their CoA, see Table 3, shows that none of the samples complied with the assay values claimed in their CoAs. Instead, three (11%) of the samples showed more than a 5% difference in assay value. In the majority of cases, the manufacturers of the finished products did not perform any testing on the API supplied. Instead, they typically rely on the CoA. This should be of concern to both regulators and manufacturers. Regulators in terms of the implementation of cGMP, while manufacturers should ethically and legally be responsible to follow cGMP for their finished products. In cases where product manufacturers perform tests on the APIs, when assay values of API are found to be lower than the prescribed limits, instead of rejecting the raw material or API, they typically use higher quantities in the production of ibuprofen tablets based on their own calculations, which raises concerns over the quality of products (Hussein S 2016, personal communication, November 8).

Our findings show a general failure of the current system of drug regulation in Pakistan that surrounds the quality of APIs used for drug production. This is in line with previous publications [5]. This will negatively impact on the quality of finished generic products for use in patients and will potentially compromise patient care. The results also show that quality assessment of multiple source medicines should not rely on assay testing alone. Other pharmacopoeia tests are also important, especially in cases where the optical activity and the presence of genotoxic, and other impurities, have a critical impact or role regarding the efficacy, safety and quality of medicines. Here, the failing sample of ibuprofen (IBU-14) passed the assay test with the highest value, while the sample failed the identification test. This invites scientific discussion regarding the value of current assay testing for generics in Pakistan, see Table 2. The results suggest that IBU-14 was not a pure API of ibuprofen. Instead, it may contain related substances or impurities which have a very close structural resemblance to the API of ibuprofen, and the HPLC method used could not identify these or discriminate them from the actual API of the drug [30]. This is why the USP does not mention the use of the HPLC method for the identification testing of ibuprofen API. Consequently, the USP compendium of methods for the identification of ibuprofen API, i.e. the FTIR and UV-Spectrophotometer methods, should be used in the future to assess the content of APIs in Pakistan.

The extra peak in the chromatograms, at 3.1 to 3.23 minutes, is also an important observation. When samples IBU-3, IBU-4, IBU-5, IBU-10, IBU-19 and IBU-25 (18.5%) were investigated for their source of manufacturing, it was found these samples were procured from only three sources. Two were in Pakistan (B and H) and one was in India (C). Further appraisal revealed that all APIs purchased from sources C and H showed this extra peak at the same time range. This illustrates the necessity to perform prequalification studies to evaluate the quality of the API from pharmaceutical manufacturers, before turning the raw materials into finished goods. However, only two out of seven (approximately 29%) API samples purchased from source B showed this extra peak. These results need to be further investigated for the characterization of this peak through evaluation of the route of synthesis or method of manufacturing of the API in order that potential corrective and preventive measures can be suggested for the future. It seems that this extra peak may be due to residual solvent or impurities remaining in the API. However, this needs further investigating before any definitive statements can be made. We are aware that both the British Pharmacopoeia and European Pharmacopoeia include a test for related substances for ibuprofen, with 18 potential impurities listed in the British Pharmacopoeia. However, as mentioned previously, the USP mentions only one specific impurity.

Assessment of the drug registration process and requirements in Pakistan

In view of the findings regarding the assessment of the current procedures concerning the registration of medicines in Pakistan, the technical requirements outlined in Box 1 are a potential way to improve the quality of medicines in Pakistan.

Currently, medicines being registered in Pakistan are not undergoing full evaluation of their safety and quality, especially in terms of their APIs [5]. Some of the suggested requirements, see Box 1, are not currently a mandatory part of the registration of medicines in Pakistan, e.g. the bioequivalence of generic medicines and even submission of the SmPC (Summary of Product Characteristics) and PIL (Patient Information Leaflet). Others, which are covered under the current rules and procedures, are also not being completely fulfilled, such as performing stability studies and validation studies. Ethically and legally, applicants should be bound to fulfill these commitments and thus perform these studies before marketing their medicines. However, in reality very few companies are complying with these commitments and performing such studies before marketing their medicines (S Hussein personal communication). There was a recent incidence of counterfeit medicines at the Punjab Institute of Cardiology which is thought to be a direct result of such deficiencies in the registration process and negligence in following cGMP [31, 32].

Despite these concerns, pharmaceutical manufacturers in Pakistan currently appear reluctant to perform additional tests or provide more comprehensive information about their medicines, during and after registration. This is thought to be due to the potential negative impact this could have on business (S Hussein, personal communication). In fact, the reverse may be true which would lead to improvement in the quality of generics for consumption in Pakistan, and a greater potential for export to other countries.

Here we outline a number of recommendations that should be considered by the Pharmaceutical Evaluation and Registration (PE & R) Division within DRAP, in consultation with Pakistani pharmaceutical companies, to improve the quality of generics produced by domestic manufacturers for use in Pakistan as well as for exportation.

These include a stepwise plan for the implementation of CTDs and new requirements in line with ICH standards, over one to three years, for example:

Alternatively:

Recently, the efforts of DRAP, in collaboration with USP and WHO, to develop the ‘Road Map for Strengthening the Registration System of Pharmaceutical Products and Biologicals for Human/Veterinary Use in Pakistan’, demonstrates a noticeable step towards improving the quality of medicines in Pakistan. We will be monitoring its progress and making additional recommendations if necessary.

Together with this, there is the ongoing process that seeks to convince pharmaceutical companies through discussions, seminars, and dialogue, of the need to adopt these new requirements for drug registration, to improve patient care and the potential for drug exports. The experiences of other countries that have started to accept such registration dossiers on CTD or e-CTD (Electronic Common Technical Document), should also be communicated within Pakistan to enhance acceptance of updated requirements. These countries include: Australia, Canada, China, Croatia, Japan, Saudi Arabia, Singapore, South Africa, Switzerland, the US, and all EU Member States [33]. In addition, comparison with the pharmaceutical manufacturing industry in Jordan whose population is only eight million compared with 201 million in Pakistan. Jordan currently has 16 pharmaceutical units compared with over 600 units in Pakistan [26, 34]. However, their exports are high with over 80% of produced medicines currently being exported over 60 countries [34, 35]. This includes more than US$4.5 billion alone to Saudi Arabia [35]. In contrast, Pakistani manufacturers in 2013 only exported US$1 billion due to concerns with poor quality [25, 36].

The implementation of ICH Standards should also be applicable to already registered medicines. These improvements may be achieved in the same stepwise manner as described above at the time of their application for renewal of registration starting over the coming year.

Other recommendations may include:

Manufacturers and DRAP may consider the following technical aspects whilst undergoing prequalification of API sources:

If these measures are adopted, patients can expect good quality generics in the future. This is important, given the extent to which medicines in Pakistan are self-pay. Without such measures, patient care using generics and trust in the healthcare system will continue to be compromised, and there will be increased potential for adverse drug reactions [37]. Successful steps have already been taken to address concerns over counterfeit medicines in Pakistan, which need to continue [38]. The above considerations should be the next step to further improve the availability of safe, effective and affordable medicines in Pakistan. This is of great importance given the increasing prevalence of chronic illnesses and diseases in this country, where every third person over the age of 40 is vulnerable to a wide range of diseases [39], and 70% of the population lives on less than US$2 per day [40].

The results of this study document the concerns over the current regulations for assessment of the quality of drug raw materials (APIs) in Pakistan. These need to be urgently addressed to ensure good quality generics in Pakistan for patients, and to improve potential export opportunities. The adoption of WHO and ICH recommended CTD format and WHO prequalification guidelines, to improve the process of registration of medicines in Pakistan, should help improve the current system for registering medicines. Thus, this will enhance the availability of safe, effective and cost-effective generics for patients in Pakistan and other regions. This is starting to happen and will be monitored.

Competing interest: The authors declare that they have no conflicts of interest apart from those stated. No writing assistance was utilized in the production of this manuscript. The write-up of this paper was in part sponsored by the Karolinska Institutet.

Provenance and peer review: Not commissioned; externally peer reviewed.

Babar Khan1, BPharm, MPH, PhD

Brian Godman2,3, BSc, PhD

Ayesha Babar1, BPharm, MPhil

Shahzad Hussain4, BPharm, MPhil

Sidra Mahmood5, PharmD, MSc

Tahir Aqeel1, BPharm, MPhil

1Department of Pharmacy, University of Lahore, Jinnah Avenue, Islamabad Campus, Pakistan

2Department of Laboratory Medicine, Division of Clinical Pharmacology, Karolinska Institute, Karolinska University Hospital Huddinge, SE-14186 Stockholm, Sweden

3Strathclyde Institute of Pharmacy and Biomedical Sciences, Strathclyde University, Glasgow G4 ORE, UK

4National Institute of Health, House No. C13, NIH Colony, Chak Shahzad, Park Road, Islamabad, Pakistan

5Scotman Pharmaceuticals Pvt Ltd, 1-10/3, Industrial Area, Islamabad – 4400, Pakistan

References

1. Chowdhry NJ. Growth challenges of pharmaceutical industry in Pakistan. PPMA. Available from: http://health-asia.com/conferences/2014/Presentations/Day1/PharmaConvention/02-Nasir-javaid.pdf

2. European Commission (EC) Trade-related Technical Assistance Programme (TRTA) for Pakistan [homepage on the Internet]. [cited 2016 Nov 8]. Available from: http://www.tradecapacitypakistan.com/new/pdf/itc/SS2.pdf

3. Hafeez-Ur-Rehman. Manual of drug laws 2010. 2nd ed. Karachi: Pioneer Book House; 2010. 216-253.

4. Manual of Drug Laws. The Drug Act, 1976 [homepage on the Internet]. [cited 2016 Nov 8]. Available from: http://medisure.com.pk/drug_law/DrugAct+Rules/index.htm

5. Zaidi S, Bigdeli M, Aleem N, Rashidian A. Access to essential medicines in Pakistan: policy and health systems research concerns. PloS One. 2013;8(5):e63515.

6. World Health Organization. WHO good manufacturing practices for pharmaceutical products: main principles. Annex 2 [homepage on the Internet]. [cited 2016 Nov 8]. Available from: http://www.who.int/medicines/areas/quality_safety/quality_assurance/TRS986annex2.pdf

7. Jamshed SQ, Hassali MA, Ibrahim MI, Babar ZU. Knowledge attitude and perception of dispensing doctors regarding generic medicines in Karachi, Pakistan: a qualitative study. J Pak Med Assoc. 2011;61(1):80-3.

8. Jamshed SQ, Ibrahim MI, Hassali MA, Masood I, Low BY, Shafie AA, et al. Perception and attitude of general practitioners regarding generic medicines in Karachi, Pakistan: a questionnaire based study. South Med Rev. 2012;5(1):22-30.

9. Riaz H, Godman B, Hussain S, Malik F, Mahmood S, Shami A, Bashir S. Prescribing of bisphosphonates and antibiotics in Pakistan: challenges and opportunities for the future. J Pharm Health Serv Res. 2015;6:111-21.

10. Shrank WH, Hoang T, Ettner SL, Glassman PA, Nair K, DeLapp D, et al. The implications of choice: prescribing generic or preferred pharmaceuticals improves medication adherence for chronic conditions. Arch Intern Med. 2006;166(3):332-7.

11. Corrao G, Soranna D, La Vecchia C, Catapano A, Agabiti-Rosei E, Gensini G, et al. Medication persistence and the use of generic and brand-name blood pressure-lowering agents. J Hypertens. 2014;32(5):1146-53.

12. Simoens S, Sinnaeve PR. Patient co-payment and adherence to statins: a review and case studies. Cardiovasc Drugs Ther. 2014;28(1):99-109.

13. Kesselheim AS, Misono AS, Lee JL, Stedman MR, Brookhart MA, Choudhry NK, et al. Clinical equivalence of generic and brand-name drugs used in cardiovascular disease: a systematic review and meta-analysis. JAMA. 2008;300(21):2514-26.

14. Gagne JJ, Choudhry NK, Kesselheim AS, Polinski JM, Hutchins D, Matlin OS, et al. Comparative effectiveness of generic and brand-name statins on patient outcomes: a cohort study. Ann Internal Med. 2014;161(6):400-7.

15. Paton C. Generic clozapine: outcomes after switching formulations. Br J Psychiatry. 2006;189(2):184–5.

16. Veronin MA. Should we have concerns with generic versus brand antimicrobial drugs? A review of issues. J Pharm Health Serv Res. 2011;2(3):135-50.

17. Godman B, Wilcock M, Martin A, Bryson S, Baumgärtel C, Bochenek T, et al. Generic pregabalin; current situation and implications for health authorities, generics and biosimilars manufacturers in the future. Generics and Biosimilars Initiative Journal (GaBI Journal). 2015;4(3):125-35. doi:10.5639/gabij.2015.0403.028

18. Corrao G, Soranna D, Arfe A, Casula M, Tragni E, Merlino L, et al. Are generic and brand-name statins clinically equivalent? Evidence from a real data-base. Eur J Intern Med. 2014;25(8):745-50.

19. Baumgärtel C, Godman B, Malmström R, Andersen M, et al. What lessons can be learned from the launch of generic clopidogrel? Generics and Biosimilars Initiative Journal (GaBI Journal). 2012;1(2):58-68. doi:10.5639/gabij.2012.0102.016

20. Godman B, Baumgärtel C. Are generic immunosuppressants safe and effective? BMJ. 2015;350:h3248.

21. The Gazette of Pakistan. 13 November 2012 [homepage on the Internet]. [cited 2016 Nov 8]. Available from: www.na.gov.pk/uploads/documents/1352964021_588.pdf

22. International Council for Harmonisation of Technical Requirements for Pharmaceuticals for Human Use (ICH). ICH guidelines [homepage on the Internet]. [cited 2016 Nov 8]. Available from: http://www.ich.org/products/guidelines.html

23. International Council for Harmonisation of Technical Requirements for Pharmaceuticals for Human Use (ICH). CDT. M4 : The common technical document [homepage on the Internet]. [cited 2016 Nov 8]. Available from: http://www.ich.org/products/ctd.html

24. Ramesh T, Saravanan D, Khullar P. Regulatory perspective for entering global pharma markets. Pharma Times. 2011;43(9):15-20.

25. Ikram J. Manufacturers say export of medicines declining. DAWN. 4 July 2015.

26. Drug Regulatory Authority of Pakistan. Updated list of pharmaceuticals manufacturers [homepage on the Internet]. [cited 2016 Nov 8]. Available from: www.dra.gov.pk/

27. Aamir M, Khalid Zaman. Review of Pakistan pharmaceutical industry: SWOT analysis. Int J Bus Inform Tech. 2011;1(1):114-7.

28. Analgesics in Pakistan. Euromonitor International. Sep 2016.

29. U.S. Pharmacopeial Convention. USP Ibuprofen updated list of pharmaceuticals manufacturers [homepage on the Internet]. [cited 2016 Nov 8]. Available from: http://www.usp.org/sites/default/files/usp_pdf/EN/USPNF/errata467Ibuprofen.pdf

30. Zolner W. Critical aspects of HPLC. Eagle Analytical Services. November 2014.

31. 2012 Pakistan fake medicine crisis. Medicines. 25 July 2012.

32. Rias A. Pharmaceuticals: drug or poison. theHealth. 2012;3(2):36-8.

33. Implementation status of CTD, eCTD, and paper-free submissions: a global overview. Thomson Reuters.

34. The Jordanian Association of Pharmaceutical Manufacturers [homepage on the Internet]. [cited 2016 Nov 8]. Available from: http://www.japm.com/Public/English.aspx?Lang=2&Page_Id=194&Menu_ID=6&Menu_Parent_ID=-1&type=R

35. Jordan Economic and Commerce Bureau [homepage on the Internet]. [cited 2016 Nov 8]. Available from: http://www.jordanecb.org/Public/English.aspx?Site_Id=1&Page_Id=551&menu_id=38

36. Indian Council for Research on International Economic Relations. Ahmed V, Batool S. India-Pakistan trade: a case study of the pharmaceutical sector. Working paper 291 [homepage on the Internet]. [cited 2016 Nov 8]. Available from: http://www.slideshare.net/vahmed/indiapakistan-trade-a-case-study-of-the-pharmaceutical-sector

37. Mahmood KT, Amin F, Tahir M, Haq IU. A need for best patient care in Pakistan. A review. J Pharm Sci & Res. 2011;3(11);1566-84.

38. Stopping fake drugs from Pakistan is too late for victims. Bloomberg.

39. Riaz H, Godman B, Bashir S, Hussain S, Mahmood S, Malik F, et al. Evaluation of drug use indicators for non-communicable diseases in Pakistan. Acta Pol Pharm. 2016;73(3):787-94.

40. Shaikh BT, Ejaz I, Mazhar A, Hafeez A. Resource allocation in Pakistan’s health sector: a critical appraisal and a path toward the Millennium Development Goals. World Health Popul. 2013;14(3):22-31.

|

Author for correspondence: Brian Godman, BSc, PhD, Strathclyde Institute of Pharmacy and Biomedical Sciences, University of Strathclyde, Glasgow G4 0RE, UK; Division of Clinical Pharmacology, Karolinska Institute, Karolinska University Hospital Huddinge, SE-14186 Stockholm Sweden |

Disclosure of Conflict of Interest Statement is available upon request.

Copyright © 2016 Pro Pharma Communications International

Permission granted to reproduce for personal and non-commercial use only. All other reproduction, copy or reprinting of all or part of any ‘Content’ found on this website is strictly prohibited without the prior consent of the publisher. Contact the publisher to obtain permission before redistributing.

Source URL: https://gabi-journal.net/assessment-of-active-pharmaceutical-ingredients-in-drug-registration-procedures-in-pakistan-implications-for-the-future.html

Author byline as per print journal: Christoph Baumgärtel, MD, MSc; Brian Godman, BSc, PhD

|

Abstract: |

Submitted: 29 September 2015; Revised: 19 October 2015; Accepted: 19 October 2015; Published online first: 2 November 2015

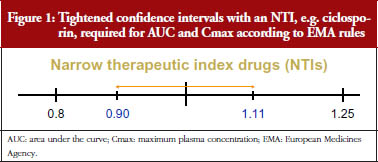

Regulatory bioequivalence rules for usual generics are well established and already recognized. However, for narrow therapeutic index drugs and immunosuppressives, there are specific and tighter criteria in place.

Drugs with a narrow therapeutic index are defined by a narrow distance between the dosage that induces a desired effect and that dosage which already has a toxic effect. Typically, this ratio in the field of pharmacology is indicated by the quotient of LD50/ED50 (LD50 = the dose at which 50% of the animals die, ED50 = the dose at which 50% of the animals show the desired effect). Alternatively, the quotient of LD5/ED95 can be used, which can better illustrate a non-linear dose-response curve.

For a perfectly safe drug, the ratio should therefore be very high. If in contrast the ratio is low, i.e. if a drug shows a value of only 3 or 4, this is called a ‘narrow therapeutic index drug’ (NTI), which must always be dosed with particularly high accuracy. Even a minor variation in plasma levels may lead sometimes to treatment failure on the one hand or inevitably to toxic effects on the other. Examples of such agents typically include immunosuppressants, digitalis, theophylline and some anti-epileptic drugs.

The acceptance range of bioequivalence trials which is usually applied for a marketing authorization of a generic drug is 80–125% of the 90% confidence interval of the ratio of the test and reference products’ AUC (area under the curve) and Cmax (maximum plasma concentration). For drugs with a narrow therapeutic index, and especially for immunosuppressives, the European Medicines Agency (EMA) demands even greater accuracy in justified cases and therefore has set more stringent criteria. This is despite in practice ratios for authorized conventional generics usually differ on average by only three to four per cent from their originator [1–4].

EMA’s overhauled bioequivalence guideline [5], in force since 2010, requires that for potential narrow therapeutic index drugs the EMA’s Pharmacokinetic Working Party (PKWP) [6] will evaluate if a generic drug newly submitted for authorization is to be thought of as an NTI and whether for this NTI actually stricter bioequivalence criteria have to be applied. It is important for a pharmaceutical manufacturer or applicant to know that there is no precasted list that names all such agents, but that all agents submitted for generic drug authorization will be evaluated by the authority on a case-by-case basis with regard to their NTI requirements.

Examples where this has already been practised are the regulatory requirements for ciclosporin and tacrolimus generics as described in a PKWP Questions and Answers document published on the EMA website [7]. In the case of these two immunosupressives, restricted bioequivalence criteria were set.

For ciclosporin, narrower acceptance intervals of 90.00–111.11% are required for both the AUC and the Cmax. Whereas, for tacrolimus the narrow acceptance interval is only required for the AUC but is not required for the Cmax. This is because tacrolimus plasma levels show accumulation with repeated dosing, resulting in a lower relevance being given to differences in initial peak plasma concentrations..

The narrower acceptance range limits for the confidence intervals for NTIs, see Figure 1, provide a greater confidence in the true bioequivalence for these drug substances. However, this requirement significantly increases the number of subjects necessary for the bioequivalence studies. Tacrolimus, for example, is a drug which is not merely an NTI, but additionally shows relatively high intra-individual variation in plasma levels. It has a relatively high coefficient of variation, close to 30%, which would classify it as a highly variable drug. Even in bioequivalence trials of tacrolimus, when a conventional acceptance range is applied, this would typically necessitate enrolling substantially higher numbers of trial participants than in the usual, bioequivalence guideline requiring a minimum of 12 to 24 subjects. One would need at least 40 subjects for a tacrolimus product, and in fact to demonstrate compliance with EMA’s mandatorily required narrower acceptance limits, it might require up to 200 to 300 subjects.

To increase the safety of generic immunosuppressives even more, it is also recommended that the summary of product characteristics (SPC) states that patients who are prescribed either a generic immunosuppressant after an originator or are switched in any other way, have their plasma levels monitored during the time of the switch to avoid potential rejection [8]. This is however similar to what is undertaken in normal clinical practice when patients are first placed on an immunosuppressant after receiving a solid organ graft.

Because of the issues concerning generic immunosuppressive medicines, Molnar et al. recently undertook a systematic review and meta-analysis of all available studies since 1980 comparing generic with originator (innovator) immunosuppressive medicines [9]. The authors documented that acute rejection was rare in transplant patients given generic immunosuppressive medicines and the incidence of rejection did not differ between the groups. However, as recently stated, the methodological standard of the published studies included was very variable and follow-up times were short [10].

In the evaluation of the pooled pharmacokinetic data, Molnar et al. showed that the generics met the US Food and Drug Administration (FDA) bioequivalence criteria, but did not all meet the stricter EMA criteria [9]. It appears that the small number of patients in some of the included studies, and as a result the wide confidence intervals, significantly contributed to this finding. For statistical reasons, in order for results to meet the stricter acceptance criteria for immunosuppressives, requiring narrow confidence intervals, a sufficiently higher number of patients must be included in the trials [11].

This effect on subject numbers needed is illustrated by the wide confidence intervals found in immunosuppressive studies with less than 20 subjects. As reviewed in the paper by Molnar et al., only trials with approximately 50 to 70 patients were able to fulfil the EMA acceptance criteria [9]. In detail, their sub-analysis of two randomized kidney trials showed that with a mean of 30 subjects, both failed to fulfil the stricter EMA bioequivalence criteria, whereas the pooled sub-analysis of seven non-randomized interventional kidney studies with a 53% higher mean sample size of 46 patients did fulfil these criteria.

Notably, the mean ratios of the test and reference products’ AUC and Cmax in most of the reported trials were well within the expected range [12]; and were in fact only a few percentage points higher or lower than 100% [9]. These data strongly suggest that there are no clinically important problems with generic immunosuppressive agents, especially with those that meet the EMA criteria, but rather that there are problems with the scientific value, relevance and interpretation of smaller studies.

It should also be noted that EMA’s precautious narrowing of bioequivalence limits was specifically implemented for situations where it is suspected that plasma level monitoring will – against the SPC advice – not be complied with; such as following a switch from an originator to a generic drug [7]. This narrowing can therefore be seen as a ‘safety net’ for the use of immunosuppressive generics. This suggests that generic immunosuppressive drugs, used in the correct manner by practitioners aware of their precautions, especially the requirement for monitoring of plasma levels at the time of switching, may indeed be considered to be bioequivalent and expected to produce outcomes that are similar to those produced by originator products.

This expectation is supported by the fact that generic versions of immunosuppressive medicines, i.e. ciclosporin, have been on the market in Europe for more than 10 years and authorities’ pharmacovigilance systems have not identified any serious issues specific for generic immunosuppressives, even after an estimated hundreds of thousands of prescribed and dispensed doses. This should alleviate major concerns among clinicians and patients when considering or undertaking a switch. However, it is expected that further well-designed studies with a suitable number of patients will help to fully address any remaining concerns with generic immunosuppressives. Further education among physicians about the need to reliably moni tor blood levels in patients when first prescribed generic immunosuppressives will also be needed. Such activities may also help to enhance adherence to immunosuppressive medicines, which is a crucial concern in transplant patients [13].

Competing interest: None.

Provenance and peer review: Not Commissioned; externally peer reviewed.

Christoph Baumgärtel, MD, MSc, Senior Scientific Expert, Coordination Point to Head of Agency, AGES Austrian Medicines and Medical Devices Agency and Austrian Federal Office for Safety in Health Care, EMA European Expert, Vice Chair of Austrian Prescription Commission, 5 Traisengasse, AT-1200 Vienna, Austria

References

1. American Medical Association. Featured report: generic drugs (A-02), June 2002 AMA Annual Meeting [homepage on the Internet]. [cited 2015 Oct 19]. Available from: http://www.ama-assn.org/ama/pub/about-ama/our-people/ama-councils/council-science-public-health/reports.page?

2. Henney JE. From the Food and Drug Administration. JAMA. 1999;282(21):1995

3. Nwakama PE. Generic drug products demonstrate small differences in bioavailability relative to brand name counterparts: Review of approved ANDAs, FDA. 2015

4. Davit BM, et al. Comparing generic and innovator drugs: a review of 12 years of bioequivalence data from the United States Food and Drug Administration. Ann Pharmacother. 2009;43(10):1583-97.

5. European Medicines Agency. Committee for Medicinal Products for Human Use (CHMP). Guideline on the investigation on bioequivalence. EMA: CPMP/EWP/QWP/1401/98 Rev. 1. January 2010 [homepage on the Internet]. 2010 Mar 10 [cited 2015 Oct 19]. Available from: http://www.ema.europa.eu/docs/en_GB/document_library/Scientific_guideline/2010/01/WC500070039.pdf

6. European Medicines Agency. Pharmacokinetics Working Party [homepage on the Internet]. [cited 2015 Oct 19]. Available from: http://www.ema.europa.eu/ema/index.jsp?curl=pages/contacts/CHMP/people_listing_000070.jsp&mid=WC0b01ac05802327c9

7. European Medicines Agency. Committee for Medicinal Products for Human Use (CHMP). Questions & answers: postitions on specific questions addressed to the Pharmacokinetics Working Party (PKWP). EMA/618604/2008 Rev. 12. 25 June 2015 [homepage on the Internet]. 2015 Jul 20 [cited 2015 Oct 19]. Available from: http://www.ema.europa.eu/docs/en_GB/document_library/Scientific_guideline/2009/09/WC500002963.pdf

8. Austrian Federal Office for Safety in Health Care. Austrian Medicines and Medical Devices Agency. Available from [homepage on the Internet]. [cited 2015 Oct 19]. Available from: https://aspregister.basg.gv.at/aspregister/

9. Molnar AO, et al. Generic immunosuppression and solid organ transplantation: systematic review and meta-analysis. BMJ. 2015;350:h3163.

10. Godman B, Baumgärtel C. Are generic immunosuppressants safe and effective? BMJ. 2015;350:h3248.

11. Baumgärtel C. [Bioequivalence – narrow therapeutic index drugs]. Bioäquivalenz – Arzneimittel mit enger therapeutischer Breite. ÖAZ, Österreichische Apotheker Zeitung. 2012;66(23):60-1. German.

12. Baumgärtel C. Myths, questions, facts about generic drugs in the EU. Generics and Biosimilars Initiative Journal (GaBI Journal). 2012;1(1):34-8. doi:10.5639/gabij.2012.0101.009

13. Tong A, Howell M, Wong G, Webster AC, Howard K, Craig JC. The perspectives of kidney transplant recipients on medicine taking: a systematic review of qualitative studies. Nephrol Dial Transplant. 2011;26(1):344-54.

|

Author for correspondence: Brian Godman, BSc, PhD, Division of Clinical Pharmacology, Karolinska Institutet, Karolinska University Hospital Huddinge, SE-14186 Stockholm, Sweden |

Disclosure of Conflict of Interest Statement is available upon request.

Copyright © 2015 Pro Pharma Communications International

Permission granted to reproduce for personal and non-commercial use only. All other reproduction, copy or reprinting of all or part of any ‘Content’ found on this website is strictly prohibited without the prior consent of the publisher. Contact the publisher to obtain permission before redistributing.

Source URL: https://gabi-journal.net/bioequivalence-of-narrow-therapeutic-index-drugs-and-immunosuppressives.html

Author byline as per print journal: Brian Godman, BSc, PhD; Michael Wilcock, MPharm; Andrew Martin, MPharm; Scott Bryson, MSc, MPH; Christoph Baumgärtel, MD; Tomasz Bochenek, MD, MPH, PhD; Winne de Bruyn, BSc; Ljiljana Sović Brkičić, MPharm; Marco D’Agata, MSc; Antra Fogele, PhD; Anna Coma Fusté, MSc; Jessica Fraeyman, PhD; Jurij Fürst, MD; Kristina Garuoliene, MD, PhD; Harald Herholz, MD, MPH; Mikael Hoff mann, MD, PhD; Sisira Jayathissa, MBBS, MMedSc (Clin Epi), MD, FRCP (Lond, Edin), FRACP, FAFPHM, FNZCPHM, DClinEpi, DOPH, DHSM, MBS; Hye-Young Kwon, BPharm, MPH, PhD; Irene Langner, MA; Marija Kalaba, MD; Eva Andersén Karlsson, MD, PhD; Ott Laius, PhD; Vanda Markovic-Pekovic, PhD; Einar Magnusson, MD; Stuart McTaggart, MSc; Scott Metcalfe, MBChB, DComH, FAFPHM (RACP), FNZCPHM; Hanne Bak Pedersen, MD; Jutta Piessnegger, PhD; Anne Marthe Ringerud, MPharm; Gisbert W Selke, BSc; Catherine Sermet, MD; Krijn Schiffers, BSc; Peter Skiold, MSc; Juraj Slabý, MD; Dominik Tomek, Pharm Dr, PhD, MPH; Anita Viksna, PhD; Agnes Vitry, PhD; Corinne Zara, MSc; Rickard E Malmström, MD, PhD

|

Introduction: The manufacturer of pregabalin has a second use patent covering prescribing for neuropathic pain – its principal indication. The manufacturer has threatened legal action in the UK if generic pregabalin rather than Lyrica is prescribed for this indication. No problems exist for practitioners who prescribe pregabalin for epilepsy or generalized anxiety disorder. This has serious implications for health authorities. In Germany, however, historically generics can be legally prescribed for any approved indication once one indication loses its patent. |

Submitted: 27 March 2015; Revised: 11 June 2015; Accepted: 24 August 2015; Published online first: 7 September 2015

The increased use of generic medicines is essential to sustain healthcare systems given the ever-increasing pressure on resources [1–4]. Prices of generic drugs are as low as 2–10% of pre-patent loss prices in some countries [5–7]. Consequently, increased use of generic drugs can generate substantial savings, which can be redirected into funding new valued high-priced medicines [2, 5–12], which is especially important for countries struggling to fund these medicines. A number of strategies globally have been initiated to encourage prescribing and dispensing of generic drugs rather than the originator (brand-name) drug, as well as patented products in a class in which all medicines are seen as essentially similar at therapeutically equivalent doses [4, 8–12].

Increasing use of generic drugs does not appear to compromise care, and many studies have reported little or no difference in outcomes across a range of products and classes [13–18]. In Europe, only generic drugs produced in accordance with the European Medicines Agency’s strict guidelines and definitions [19] are granted marketing authorization.

Well-known and agreed exceptions to generics prescribing or substitution include lithium, theophyllines, some anti-epileptic drugs, modified release preparations and immunosuppressants. In these cases, brand-name prescribing is endorsed [20–23]. Agreed exceptions to generics prescribing, including medicines to treat epilepsy and prevent organ rejection, also exist in Germany and Sweden [6, 24].

A new emerging problem, however, has come to the fore in recent years, concerning the expiry of patents for medicines that have patents for more than one indication, and the threat of legal action by the manufacturer of the originator drug against physicians. This situation occurred recently in the case of pregabalin for the treatment of epilepsy and generalized anxiety disorder (GAD) when the basic patent for pregabalin expired in July 2014 in a number of European countries. The patent for its second medical use, protecting the originator drug Lyrica’s use in treating neuropathic pain, extends to July 2017 in Europe [25, 26]. In the UK, this resulted in the manufacturer of the originator drug (Lyrica) claiming patent infringement and warning doctors not to prescribe the generic drug pregabalin for neuropathic pain [26, 27]. As far as we are aware, this is the first time this has happened, and has serious implications for health authorities.

Prior to this, the originator manufacturer of Lyrica had been fined heavily for promoting gabapentin (prelude to pregabalin) off label for the treatment of neuropathic pain [28–31], although it is now recommended for this indication [32]. In addition, there have been concerns with the methodological limitation of some of the studies of pregabalin in neuropathic pain [33–35]. Pregabalin, for example, is currently not listed in the ‘Wise List’ of Stockholm Metropolitan Healthcare Region because of efficacy and safety concerns compared with other treatments for these conditions [36]. However, there are increasing concerns with the implications of the activities of second use patents with Lyrica [26, 37].

In this paper, historical developments in Germany and the UK relating to this case are examined. Personnel from regional and national health authorities from principally across Europe, and advisers to health authorities working in universities, were then surveyed to ascertain the current situation with pregabalin in their country and to determine the best strategy for maximizing savings for countries once a product loses its patent for any indication.

In the UK, the international non-proprietary name (INN) prescribing rate is over 80%, and up to 98–99% of non-contentious generic drugs, such as proton pump inhibitors, renin-angiotensin inhibitors and statins, with pharmacists not permitted to substitute an originator drug with a generic drug when the originator drug is prescribed [7, 20, 21, 38].

The UK medicines agency recently issued advice on which epilepsy drugs to prescribe by brand name (originator) and which by INN [39]. Pregabalin was considered suitable for INN prescribing [39], which was endorsed by the originator company stating ‘there will be no clinical superiority of the originator branded medicine Lyrica over generic pregabalin’ [25].

The extended patent for neuropathic pain resulted in the originator company writing to all Clinical Commissioning Groups (CCGs) in England and Health Boards in Scotland in November 2014 pointing out that generics of pregabalin were expected to be approved only for GAD and epilepsy indications, and that the prescribing of generic pregabalin for neuropathic pain could represent ‘off-label’ use. This would be considered a patent infringement constituting an unlawful act, with the originator company reserving all legal rights in this regard [25–27].

The wish of generics companies to make generic pregabalin available in the UK across all indications resulted in a court case, with the originator company as claimant and the Actavis group as the principal defendant [26, 40]. The judge in his deliberations, posted on 21 January 2015, granted Actavis the possibility to launch generic pregabalin and again stated that the best way forward was to try to ensure physicians prescribe Lyrica for the treatment of neuropathic pain and pregabalin for other conditions, including epilepsy [40, 41].

The actions of the originator company are unsurprising. In 2013, global sales of Lyrica generated US$4.6 billion for the company [40]. In the UK, sales of Lyrica increased by 53% between 2011 and 2013 to about US$310 million. It is estimated that 54% of prescriptions in September 2014 were for treating pain, of which 44% was for neuropathic pain [40]. In 2014, sales of Lyrica were GBP 250 million (US$390 million) [26].The potential loss in revenue, therefore, would hugely impact company sales – estimated to be GBP 220 million per year (US$340 million) across all indications assuming high INN prescribing rates and generic drug prices rapidly falling by 90% of the price of Lyrica [7, 42].

In an attempt to preserve sales of Lyrica, the originator company has been proactive in lobbying groups in the UK who could influence physician prescribing, such as the Medicine Management groups within CCGs, the Pharmaceutical Services Negotiating Committee, the General Practitioners Committee of the British Medical Association, and the National Health Service [26, 32, 37, 43–45]. For instance, National Health Service (NHS) England in March 2015 issued advice to all CCGs that within electronic prescription systems there should be a notice or advice box stating ‘If treating neuropathic pain, prescribe Lyrica (brand) due to patent protection. For all other indications, prescribe generically’ [45]. The Pharmaceutical Services Negotiating Committee stated to its members they should be aware that the originator company still retains the indication for neuropathic pain. Members were also made aware that following a high court decision, ‘it was agreed by all parties that the generic [drug] producers would write to CCGs to ensure they were aware that the generic [drug] could not be supplied for the patented indication. A CCG or other party that promotes the supply of generic pregabalin for the patented indication risks facing legal action’ [43].

This situation in the UK has important future implications for generics and biosimilars companies across countries, as it may impede the ability of health authorities to fully realize potential savings from generics and biosimilars once the first indication loses its patent, especially if pharmaceutical companies look to extend the number of indications for their new medicines once launched in an attempt to extend the patent life.

Germany has taken a different approach to the UK. Currently, nine pregabalin generics are available and reimbursed in Germany (up to April 2015), all of which have the indications for epilepsy and anxiety disorders. The situation, however, is now less clear cut as the originator manufacturer, has taken Ratiopharm, Hexal, 1A Pharma, Glenmark and Aliud Pharma and some Sickness Funds (German payers) to court in an attempt to conserve Lyrica sales for neuropathic pain (up to 10 April 2015) [46]. The legal battle is still ongoing. The originator company’s previous strategy to promote Lyrica was to communicate directly with physicians or via KVs (regional doctors’ associations) by letter, making it clear that Lyrica was the only pregabalin licensed for neuropathic pain [47]. However, these communications were largely dismissed by KVs because the focus was on legal rather than medical issues, and the KVs continued to advise physicians to reach targets of generics prescribing of at least 85%. In addition, the Social Code Book V (SGB V), which is decisive for Sickness Funds, stated in paragraph 129 that generics substitution is possible wherever at least one indication matches [48–50].

The contrast between the situation in the UK and the situation in Germany, and the implications for potential savings when other pharmaceutical products lose their patents for some but not all indications, has led health authorities, across Europe, to review the current status of pregabalin in other countries in order to refine their own strategies if possible.

A qualitative study was undertaken to ascertain the current situation between generic pregabalin and Lyrica among health authorities principally from across Europe. This included a range of Central, Eastern and Western European countries with different epidemiology and funding of health care, as well as policies to enhance the prescribing of generics. This builds on the situation Germany and the UK, and is in line with current recommendations for conducting cross-national research projects [51]. The aim was to maximize future savings for countries once a product loses its patent for any indication.

Personnel from 33 regional and national health authorities mainly from across Europe, and personnel from nine universities working closely as advisers to health authorities or with insight into health authority activities, were contacted by email to provide answers to the following four questions (up to April 2015):

1. Are you aware of any similar examples to the situation of pregabalin and Lyrica in the UK from other pharmaceutical companies for small molecules once the patent has been lost (biosimilars are a different issue)? If so, what were these and how were they handled (if at all).

2. Was Lyrica reimbursed in your country? If yes, for what indications?

3. Has generic pregabalin been launched in your country/about to be launched? If yes what date (month) and indications?

4. Has the originator company issued a letter to healthcare professionals in your country similar to the letter issued to CCGs in the UK? If yes, what actions (if any) are being taken?

This was supplemented with knowledge from other high-income countries taking different approaches to the availability of generic pregabalin to potentially provide additional examples.

All health authority personnel are involved with either pricing and reimbursement decisions, decisions concerning funding or monitoring the use of medicines, or both, including generics, in their countries and regions. Consequently, it was felt that they would have the most insight into the current situation concerning pregabalin and Lyrica in their countries and regions. European countries included those from Central, Eastern and Western Europe to ensure legitimacy with the findings. Personnel from regions in The Netherlands, Sweden and the UK were also included, as healthcare budgets in these countries are devolved downwards.

The written information supplied by the co-authors and others for each of the questions for each country was collated and summarized by the corresponding author. The summarized information was subsequently checked via email and face-to-face contact with the relevant co-author(s) to ensure the accuracy of the summarized information. The information supplied was subsequently summarized into five categories to improve the interpretation of the findings and the implications for the future, building on the situation in England and Germany.

The five categories included:

Potential or actual demand-side measures among the health authorities were not broken down into the ‘four Es’: education, engineering, economics and enforcement, as in our previous paper on generic clopidogrel [52]. This is because pregabalin may not be available and reimbursed across Europe and the other chosen countries.

This information was supplemented with a limited literature search for further information about generics generally, pregabalin and the activities of the originator company, including recent court cases, as well as relevant papers known to the co-authors. A similar methodological approach was used when reviewing health authority activities when generic clopidogrel became available [52].

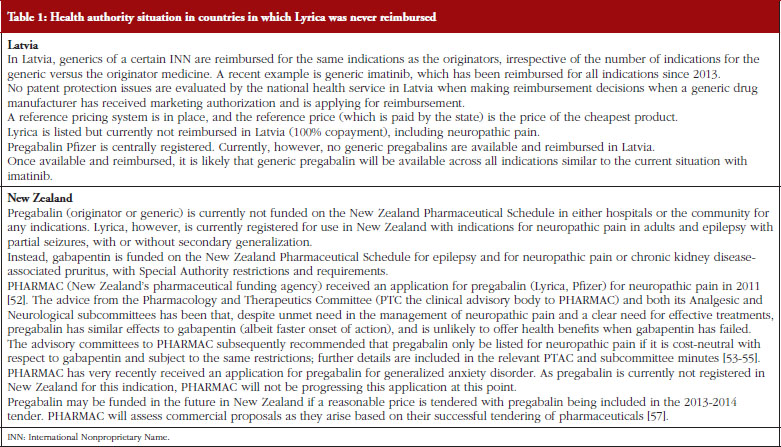

The results of the survey revealed that respondents were typically unaware of similar examples to pregabalin and Lyrica in their countries. For example, generic clopidogrel was reimbursed and endorsed by health authority personnel from across Europe despite generic clopidogrel not including all licensed indications at launch [52]. The main exception was Lithuania, see Table 2, with Glivec and generic imatinib.

The current situation for Lyrica and generic pregabalin among health authorities and health insurance companies across Europe and other selected countries is included in Tables 1–3 as well as Appendices 1 and 2. This also includes additional activities in Scotland.

In this paper, we have described the situation across Europe following the launch or imminent launch and reimbursement of generic pregabalin. We were not surprised by the activities of the originator company in the UK in view of the current high levels of INN prescribing, no clinical issues with patients being switched between generic pregabalin or Lyrica across indications, and the high sales of Lyrica globally and in the UK [7, 21, 25, 39, 40, 65].

The threat of legal action against physicians taught to prescribe generically is a major concern among health authorities already struggling to fund increased volumes and new high-priced medicines within available budgets [66]. It also raises issues about off-label prescribing generally and pharmacists checking the use of medication with every patient [37]. Moreover, it would seem that this is the first time that an originator company has threatened court cases against physicians in an extended patent use situation. Previous examples can be found in some countries such as Lithuania, see Table 2; however, no coordinated approach has been taken across countries. These concerns are exacerbated if such activities make European markets unattractive for generics companies, thereby reducing potential savings once a product loses its patent. It is also unhelpful to influence physicians to remember to prescribe different versions of the same molecule for different indications. This could, however, potentially be addressed through increasing use of electronic prescribing support systems. Actions of this nature also impede constructive working relationships between pharmaceutical companies and health service personnel [26].

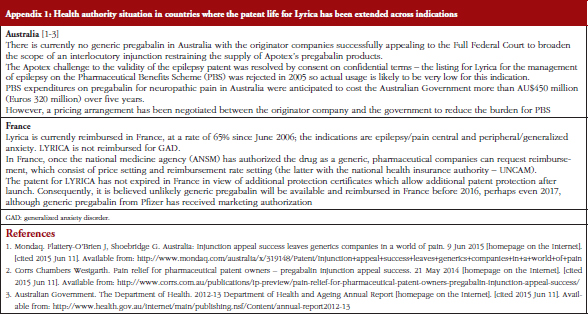

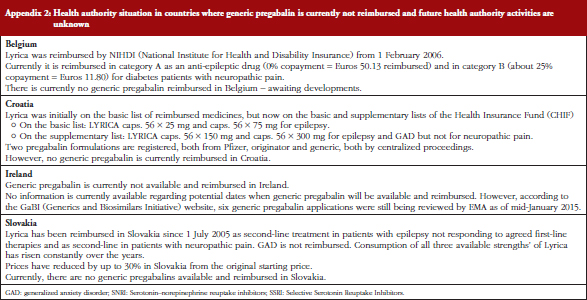

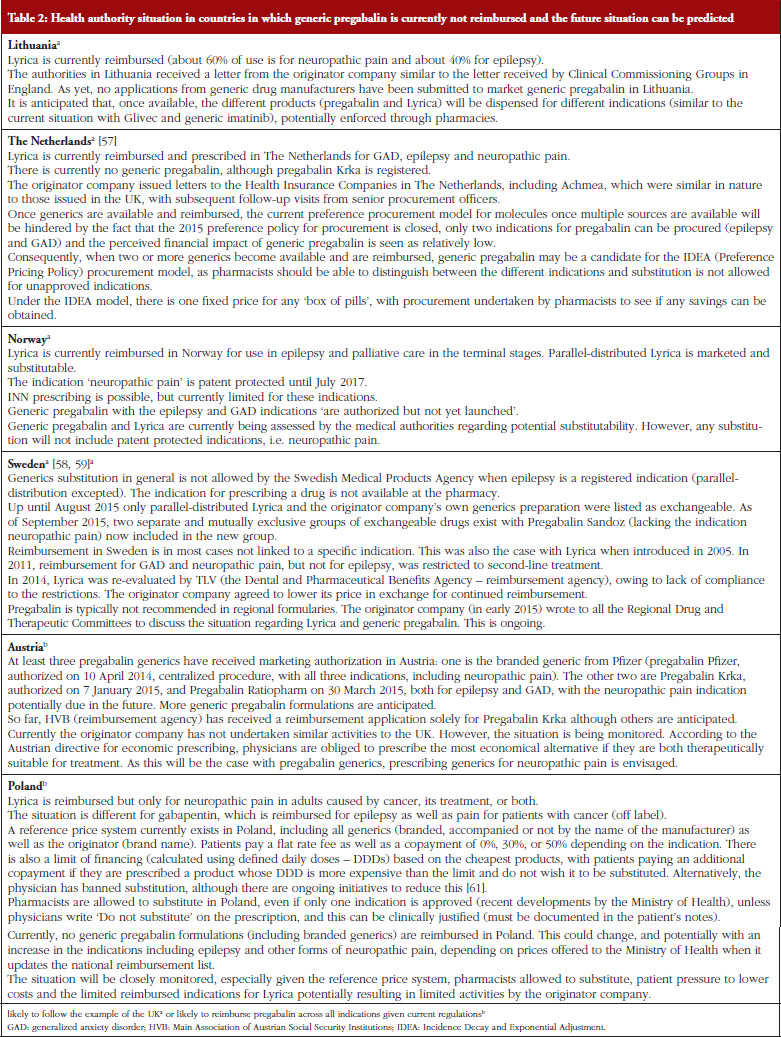

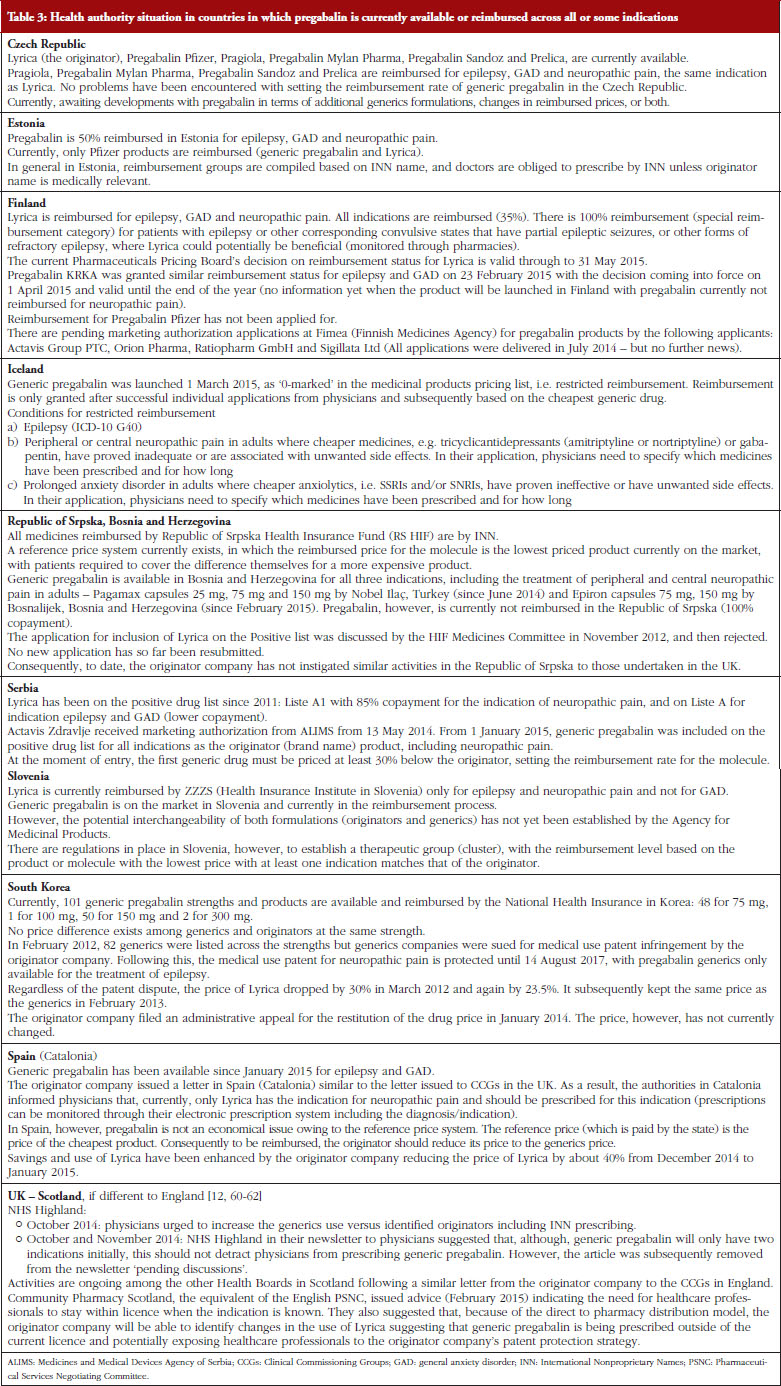

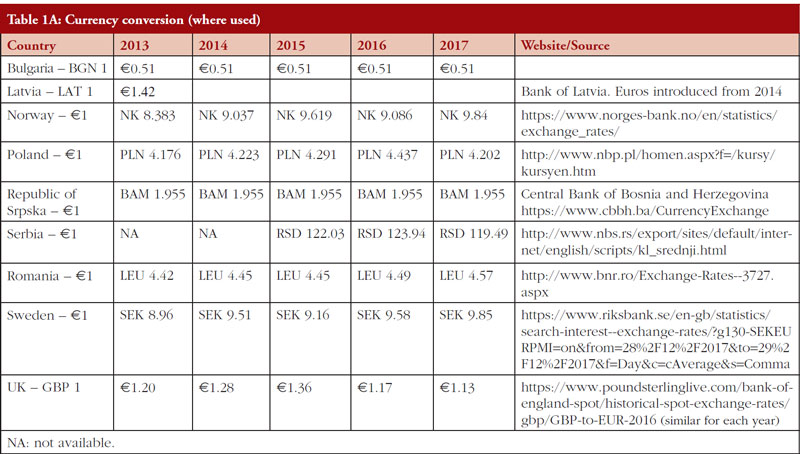

As seen in Tables 1–3, and Appendices 1 and 2, very different approaches have been taken across countries to the availability of generic pregabalin. In addition to historic approaches taken in Germany, countries such as Czech Republic, Estonia, Republic of Srpska, Bosnia and Herzegovina, and Serbia, see Table 3, are good examples of approaches taken to enhance the prescribing of pregabalin across all indications. The situation in Austria, Poland, and Slovenia will be closely monitored, see Tables 2 and 3, to see if they could also provide examples of potential ways forward to enhance the prescribing of pregabalin across all indications.

Lithuania, Norway and Sweden will also be closely monitored to see whether the originator company will be successful in limiting the prescribing of generic pregabalin in practice to epilepsy and GAD, with Lyrica prescribed and dispensed for neuropathic pain, see Table 2 and Appendix 2. Whether these countries will follow the examples of Bosnia and Herzegovina, Czech Republic, Estonia, Germany (historic), Republic of Srpska Bosnia and Herzegovina, and Serbia, see Table 3, once pregabalin is available and reimbursed remains to be seen.

It is interesting to note the different approaches taken by the originator company to the KVs in Germany initially compared with regional health authorities in England and Health Boards in Scotland, see Table 3. This acknowledges adherence to current stipulations of Social Code Book V serving as an example to other countries worried about such developments in the future, although this is now being challenged.

The introduction of reference priced systems with reimbursement typically just covering the costs of the lowest priced molecule is another way forward, given the extent of internal reference pricing across Europe once multiple sources of a product become available [1]. This works best if originator companies drop their prices to compete; alternatively, the situation is pre-empted as seen for instance in Spain, see Table 3. Alternatively, the price of the originator (brand name) is reduced over time despite the protestations of the originator manufacturer, as seen in South Korea, see Table 3. Difficulties could, potentially occur if reimbursement or substitution for one indication is not recommended, which could occur in Sweden for treatments for epilepsy, see Table 2. This has not currently been a problem in South Korea with multiple pregabalin packs available from different manufacturers, see Table 3. This situation could potentially reduce the attractiveness of the market to generics companies if originator (brand name) manufacturers are happy to drop their prices to those of generics to compete in the knowledge that patients may prefer to stay with the originator if copayments are the same in the absence of any substitution in pharmacies. This is, however, being resisted by the originator company in South Korea, see Table 3.

The developments surrounding Lyrica and generic pregabalin, including potential health authority activities to enhance the prescribing of generic pregabalin, will be closely monitored over the coming months. This will be combined with research on the resultant effect of prescribing and dispensing of pregabalin or Lyrica in practice. The objective will be to provide further guidance to health authorities with their increasing need to maximize savings from generics or biosimilars once they become available for at least one indication. This is essential to maintain the ideals of comprehensive and equitable healthcare especially in Europe.

We have documented different approaches to the availability of generic pregabalin, with countries such as Germany historically having measures in place to enhance the prescribing of generics once at least one indication is off patent. This contrasts with countries such as the UK where generic pregabalin can only be prescribed for some but not all indications. This appreciably reduces potential savings from the availability of generics, which is an increasing concern given ever growing pressures on available resources.

The situation in the UK will now be closely monitored following a recent court judgement post acceptance of the paper overturning the originator company’s patent for pregabalin for pain control; although, this is currently being challenged by the company [67].

We thank Ms Elina Asola for the current information regarding Finland, Ms Laura McCullagh and Ms Susan Spillane for the current information regarding Ireland, and Ms Marie-Camille Lenormand for information regarding France.

All authors wish to thank the English editing support provided by Ms Maysoon Delahunty, GaBI Journal Editor, for this manuscript.

There are no conflicts of interest from any author. However, the majority of authors are employed by ministries of health, health authorities and health insurance companies or are advisers to them. The content of the paper and the conclusions though are those of each author and may not necessarily reflect those of the organization that employs them.

This work was in part supported by grants from the Karolinska Institutet, Sweden.

Competing interests: None.

Provenance and peer review: Not commissioned; externally peer reviewed.

Brian Godman1,2, BSc, PhD; Michael Wilcock3, MPharm; Andrew Martin4, MPharm; Scott Bryson2,5, MSc, MPH; Christoph Baumgärtel6, MD; Tomasz Bochenek7, MD, MPH, PhD; Winne de Bruyn8, BSc; Ljiljana Sović Brkičić9, MPharm; Marco D’Agata10, MSc; Antra Fogele11, PhD; Anna Coma Fusté12, MSc; Jessica Fraeyman13, PhD; Jurij Fürst14, MD; Kristina Garuoliene15,16, MD, PhD; Harald Herholz17, MD, MPH; Mikael Hoffmann18, MD, PhD; Sisira Jayathissa19, MBBS, MMedSc (Clin Epi), MD, FRCP (Lond, Edin), FRACP, FAFPHM, FNZCPHM, DClinEpi, DOPH, DHSM, MBS; Hye-Young Kwon20,21, BPharm, MPH, PhD; Irene Langner22, MA; Marija Kalaba23, MD; Eva Andersén Karlsson24,25, MD, PhD; Ott Laius26, PhD; Vanda Markovic-Pekovic27,28, PhD; Einar Magnusson29, MD; Stuart McTaggart30, MSc; Scott Metcalfe31, MBChB, DComH, FAFPHM (RACP), FNZCPHM; Hanne Bak Pedersen32, MD; Jutta Piessnegger33, PhD; Anne Marthe Ringerud34, MPharm; Gisbert W Selke22, BSc; Catherine Sermet35, MD; Krijn Schiffers36, BSc; Peter Skiold37, MSc; Juraj Slabý38, MD; Dominik Tomek39, Pharm Dr, PhD, MPH; Anita Viksna11, PhD; Agnes Vitry40, PhD; Corinne Zara12, MSc; Rickard E Malmström41, MD, PhD

1Department of Laboratory Medicine, Division of Clinical Pharmacology, Karolinska Institutet, Karolinska University Hospital Huddinge, SE-14186 Stockholm, Sweden

2Strathclyde Institute of Pharmacy and Biomedical Sciences, University of Strathclyde, Glasgow, UK

3Head of Prescribing Support Unit, Pharmacy Department, Royal Cornwall Hospitals NHS Trust, Truro, Cornwall TR1 3LJ, UK

4North West Commissioning Support Unit (NWCSU), Salford, Manchester M6 5FW, UK

5NHS Greater Glasgow & Clyde Prescribing Management Group, Glasgow, UK

6AGES Austrian Medicines and Medical Devices Agency and Austrian Federal Office for Safety in Health Care, 5 Traisengasse, AT-1200 Vienna, Austria

7Department of Drug Management, Faculty of Health Sciences, Jagiellonian University Medical College, Krakow, Poland

8Utrecht University, Utrecht, The Netherlands

9Croatian Health Insurance Fund, 37 Branimirova, Zagreb, Croatia

10Achmea Zorg and Health, 2 Handelsweg, NL-3707 NH Zeist, The Netherlands

11The National Health Service of Latvia, 31 k-3 Cēsuiela, LV-1012 Riga, Latvia

12Barcelona Health Region, Catalan Health Service, Barcelona, Spain

13Epidemiology and Social Medicine, Research Group Medical Sociology and Health Policy, University of Antwerp, Antwerp, Belgium

14Health Insurance Institute, Ljubljana, Slovenia

15Faculty of Medicine (Department of Pathology, Forensic Medicine and Pharmacology), Vilnius University, Vilnius, Lithuania

16State Medicines Control Agency, Vilnius, Lithuania

17Kassenärztliche Vereinigung Hessen, 15 Georg Voigt Strasse, DE-60325 Frankfurt am Main, Germany

18NEPI – Nätverk för läkemedelsepidemiologi, Sweden

19Department of Medicine, Hutt Valley DHB, Lower Hutt, Wellington, New Zealand

20Institute of Health and Environment, Seoul National University, Seoul, South Korea

21Department of Global Health and Population, Harvard School of Public Health, Boston, MA, USA

22Wissenschaftliches Institut der AOK (WIdO), 31 Rosenthaler Straße, DE-10178 Berlin, Germany

23Republic Institute for Health Insurance, Belgrade, Serbia

24,25Drug and Therapeutics Committee, Unit of Medicine Support, Public Healthcare Services, Stockholm County Council and Department of Clinical Science and Education, Karolinska Institutet, Södersjukhuset, Stockholm, Sweden

26State Agency of Medicines, Tartu, Estonia

27,28Faculty of Medicine, University of Banja Luka, Banja Luka, Republic Srpska, Bosnia and Herzegovina; Ministry of Health and Social Welfare, Banja Luka, Republic Srpska, Bosnia and Herzegovina

29Department of Health Services, Ministry of Health, Reykjavík, Iceland

30Public Health and Intelligence, NHS National Services Scotland, Edinburgh EH12 9EB, UK

31PHARMAC, 40 Mercer Street, Wellington 6011, New Zealand

32Health Technologies and Pharmaceuticals, Division of Health Systems and Public Health, WHO Regional Office for Europe, Copenhagen, Denmark

33Hauptverband der Österreichischen Sozialversicherungsträger, Vienna, Austria

34Section for Reimbursement, Department for Pharmacoeconomics, Norwegian Medicines Agency, 8 Sven Oftedals vei, NO-0950 Oslo, Norway

35IRDES, 10 rue Vauvenargues, FR-75018 Paris, France

36Erasmus University, Rotterdam, The Netherlands

37Dental and Pharmaceuticals Benefits Agency (TLV), PO Box 22520, 7 Flemingatan, SE-10422 Stockholm, Sweden

38State Institute for Drug Control, Czech Republic

39Department of Pharmacology, Faculty of Medicine, Slovak Medical University, Bratislava, Slovakia

40Quality Use of Medicines and Pharmacy Research Centre, Sansom Institute, School of Pharmacy and Medical Sciences, University of South Australia, GPO Box 2471, Adelaide SA 5001, Australia

41Department of Medicine Solna, Karolinska Institutet, Clinical Pharmacology Karolinska University Hospital Solna, Stockholm, Sweden

References

1. Simoens S. A review of generic medicine pricing in Europe. Generics and Biosimilars Initiative Journal (GaBI Journal). 2012;1(1):8-12. doi:10.5639/gabij.2012.0101.004

2. Dylst P, Vulto A, Simoens S. Analysis of European policy towards generic medicines. Generics and Biosimilars Initiative Journal. 2014;3(1):34-5. doi:10.5639/gabij.2014.0301.011

3. Dylst P, Vulto A, Godman B, Simoens S. Generic medicines: solutions for a sustainable drug market? Appl Health Econ Health Policy. 2013;11(5):437-43.

4. Godman B, Abuelkhair M, Vitry A, Abdu S, Bennie M, Bishop I, et al. Payers endorse generics to enhance prescribing efficiency; impact and future implications, a case history approach. Generics and Biosimilars Initiative Journal (GaBI Journal). 2012;1(2):69-83. doi:10.5639/gabij.2012.0102.017

5. Woerkom M, Piepenbrink H, Godman B, Metz Jd, Campbell S, Bennie M, et al. Ongoing measures to enhance the efficiency of prescribing of proton pump inhibitors and statins in The Netherlands: influence and future implications. J Comp Eff Res. 2012;1(6):527-38.

6. Godman B, Wettermark B, Hoffmann M, Andersson K, Haycox A, Gustafsson LL. Multifaceted national and regional drug reforms and initiatives in ambulatory care in Sweden: global relevance. Expert Rev Pharmacoecon Outcomes Res. 2009;9(1):65-83.

7. Godman B, Bishop I, Finlayson AE, Campbell S, Kwon HY, Bennie M. Reforms and initiatives in Scotland in recent years to encourage the prescribing of generic drugs, their influence and implications for other countries. Expert Rev Pharmacoecon Outcomes Res. 2013;13(4):469-82.

8. Kaplan WA, Ritz LS, Vitello M, Wirtz VJ. Policies to promote use of generic medicines in low and middle income countries: a review of published literature, 2000-2010. Health Policy. 2012;106(3):211-24.

9. Dylst P, Vulto A, Simoens S. Demand-side policies to encourage the use of generic medicines: an overview. Expert Rev Pharmacoecon Outcomes Res. 2013;13(1):59-72.

10. Godman B, Wettermark B, van Woerkom M, Fraeyman J, Alvarez-Madrazo S, Berg C, et al. Multiple policies to enhance prescribing efficiency for established medicines in Europe with a particular focus on demand-side measures: findings and future implications. Front Pharmacol. 2014;5:106.

11. Vogler S, Zimmermann N. How do regional sickness funds encourage more rational use of medicines, including the increase of generic uptake? A case study from Austria. Generics and Biosimilars Initiative Journal (GaBI Journal). 2013;2(2):65-75. doi:10.5639/gabij.2013.0202.027

12. All professionals urged to maximise use of generics. NHS Highland. the Pink One. 2014;110 extra (Special edition).

13. Kesselheim AS, Misono AS, Lee JL, Stedman MR, Brookhart MA, Choudhry NK, et al. Clinical equivalence of generic and brand-name drugs used in cardiovascular disease: a systematic review and meta-analysis. JAMA. 2008;300(21):2514-26.

14. Kesselheim AS, Stedman MR, Bubrick EJ, Gagne JJ, Misono AS, Lee JL, et al. Seizure outcomes following the use of generic versus brand-name antiepileptic drugs: a systematic review and meta-analysis. Drugs. 2010;70(5):605-21.

15. Corrao G, Soranna D, Merlino L, Mancia G. Similarity between generic and brand-name antihypertensive drugs for primary prevention of cardiovascular disease: evidence from a large population-based study. Eur J Clin Invest. 2014;44(10):933-9.

16. Veronin M. Should we have concerns with generic versus brand antimicrobial drugs? A review of issues. JPHSR. 2011;2(3):135-50.

17. Paton C. Generic clozapine: outcomes after switching formulations. Br J Psychiatry. 2006;189:184-5.

18. Araszkiewicz AA, Szabert K, Godman B, Wladysiuk M, Barbui C, Haycox A. Generic olanzapine: health authority opportunity or nightmare? Expert Rev Pharmacoecon Outcomes Res. 2008;8(6):549-55.

19. Baumgärtel C. Myths, questions, facts about generic drugs in the EU. Generics and Biosimilars Initiative Journal (GaBI). 2012;1(1):34-8. doi:10.5639/gabij.2012.0101.009

20. Ferner RE, Lenney W, Marriott JF. Controversy over generic substitution. BMJ. 2010;340:c2548.

21. Duerden MG, Hughes DA. Generic and therapeutic substitutions in the UK: are they a good thing? Br J Clin Pharmacol. 2010;70(3):335-41.

22. Abuelkhair M, Abdu S, Godman B, Fahmy S, Malmstrom RE, Gustafsson LL. Imperative to consider multiple initiatives to maximize prescribing efficiency from generic availability: case history from Abu Dhabi. Expert Rev Pharmacoecon Outcomes Res. 2012;12(1):115-24.

23. Garuoliene K, Godman B, Gulbinovic J, Wettermark B, Haycox A. European countries with small populations can obtain low prices for drugs: Lithuania as a case history. Expert Rev Pharmacoecon Outcomes Res. 2011;11(3):343-9.

24. Gemeinsamer Bundesausschuss. Anlage VII zum Abschnitt M der Arzneimittel-Richtlinie. Regelungen zur Austauschbarkeit von Arzneimitteln (aut idem). 10 Apr 2015 [homepage on the Internet]. 2015 May 22 [cited 2015 Jun 11]. Available from: https://www.g-ba.de/downloads/83-691-376/AM-RL-VII-Aut-idem_2015-04-10.pdf

25. Pfizer threatens pharmacists, doctors if they take its name in vain. 24 Dec 2014 [cited 2015 Jun 11]. Available from: http://boingboing.net/2014/12/24/pfizer-threatens-pharmacists.html

26. What a pain. Drugs and Therapeutics Bulletin. 2015;53(5):50.

27. Noonan KE. Patent Docs Biotech & Patent Law & News Blog [Internet]. The uncomfortable intersection between the practice of medicine and reality. 29 December 2014. [cited 2015 Jun 11]. Available from: http://www.patentdocs.org/2014/12/the-uncomfortable-intersection-between-the-practice-of-medicine-and-reality.html