Author byline as per print journal: Steven Kozlowski1, MD; Ellen Tworkoski2, MS, MPhil; Carmen Dekmezian2, MS; Yanchang Zhang2, MPH; Natasha Flowers2, BA; Alvin So3, MS; Andreas M Schick3, PhD; Michael Wernecke2, BA; Thomas MaCurdy2,4, PhD; Jeffrey A Kelman5, MD, MMSc

|

Background: Drug pricing and availability are key concerns for reducing healthcare costs and meeting patient needs. There is a complex chain of manufacturers, payers, wholesalers, retailers, patients, and other parties in drug supply and reimbursement. Understanding which of these parties drive generics manufacturer choice can inform economic models and the epidemiology of generic drug use. |

Submitted: 8 August 2019; Revised: 7 September 2019; Accepted: 7 September 2019; Published online first: 20 September 2019

The passage of the Drug Price Competition and Patent Term Restoration Act (Hatch-Waxman Act) in 1984 created a pathway for generic drugs in the US. Generic drugs marketed by more than one manufacturer (multisource generic drugs) have led to lower drug prices, healthcare savings, and greater access to important therapies [1, 2]. There are opportunities to further increase access through increased competition [3]. In considering strategies to achieve this, it is important to identify how choices are made in the complex chain of manufacturers, payers, wholesalers, retailers (pharmacies), consumers (patients) and other parties, e.g. pharmacy benefit managers [4]. Thus, it is important to understand what factors are associated with the receipt of a given generic drug manufacturer’s product.

In addition to furthering understanding of generics market competition, identifying factors closely associated with manufacturer choice may improve our ability to adequately adjust for confounding of observational studies in assessing generic drug effectiveness. While systematic reviews and meta-analyses have concluded that generic and brand drugs have similar clinical outcomes [5, 6], concerns remain regarding certain generic drugs [5, 7–9] or bias in studies comparing generic and brand drugs [10]. Such concerns and the increasing number of multisource drugs will likely result in further research comparing drug manufacturers. If factors associated with receipt of a given drug manufacturer are also associated with clinical outcomes, they may confound such research, leading to inaccurate conclusions. Therefore, these factors should be understood and considered in study designs and analyses.

We considered factors that have been shown to impact drug market access. Previous research has linked geographic location to an individual’s economic or physical access to medications [11, 12]. Pharmacy chain may also impact the availability of drugs [13]. Insurance plans, such as Medicare Part D, impact access [14] and may also impact specific drug availability through pricing, formularies, preferred pharmacies, and preferred drugs. We studied the association between manufacturer and each of these factors, as they could all potentially impact outcomes as well as access.

Data source and cohort formation

Medicare Part D claims were used for all analyses. The main study population included all beneficiaries receiving prescriptions for the specified generic drugs in 2014. A secondary analysis of the duration of manufacturer associations included brand and generic drug prescriptions from 2010 through 2014. As this study focused on prevalent associations between variables impacting drug market access and generic drug manufacturer, no other population restrictions were applied. This study was determined to meet the requirements of a Public Health Surveillance activity by the US Food and Drug Administration (FDA)/Center for Drug Evaluation and Research Human Subject Protection Liaison to the FDA Institutional Review Boards (IRB). The analyses utilize only existing records and the subjects cannot be identified.

Drug exposure

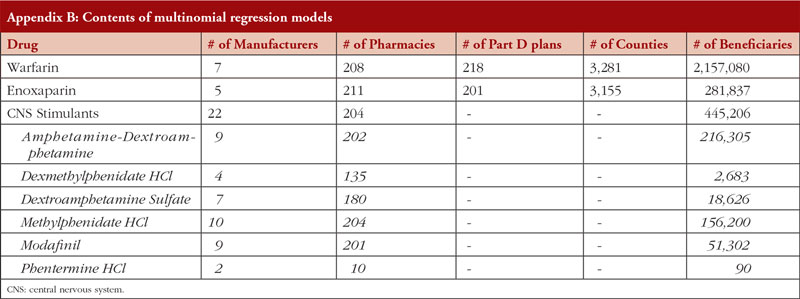

Generic warfarin and enoxaparin were selected for initial evaluation, as they are widely used anticoagulants with multiple generic drug manufacturers. In order to identify potential associations in manufacturer choice among medications that are commonly co-prescribed, a set of generic cardiovascular drugs were evaluated together in the context of specific pharmacy chains. These included enoxaparin and warfarin in addition to the beta blockers carvedilol and atenolol, the antihyperlipidemic pravastatin sodium, and the antiarrhythmic amiodarone HCl. To determine the generalizability of identified associations across medications, the study was subsequently expanded to include a set of six multisource generic central nervous system (CNS) stimulants with indications for attention-deficit/hyperactivity disorder (ADHD), obesity and narcolepsy. These included amphetamine-dextroamphetamine, dexmethylphenidate, dextroamphetamine sulfate, methylphenidate, modafinil, and phentermine. National Drug Codes (NDCs) corresponding to the non-proprietary drug names of interest, as characterized by the Medi-Span Generic Product Identifier code at level 4 (GPI4), were used to identify claims for all drugs. See Appendix A for additional information on selection and identification of drugs in this study.

Factors evaluated and outcome

Medicare beneficiaries’ county of residence was identified via the Federal Information Processing Standard (FIPS) codes listed on Part D claims. Beneficiaries’ Part D Medicare plan was assessed at the level of the plan’s parent organization, rather than the specific plan, as this would identify plan sponsor-generic drug manufacturer associations. The parent organization was identified by mapping the contract number listed on Part D claims to the Plan Directory for Medicare Prescription Drug Plans provided by the Center for Medicare and Medicaid Services (CMS).

The dispensing pharmacy chain for each prescription was identified via the National Provider Identifier (NPI) listed on the Part D claim. NPIs were mapped to pharmacy chain names using the National Plan and Provider Enumeration System (NPPES) database. For independent or privately-owned pharmacies, the pharmacy name was used in place of a chain name. Some text cleaning of chain names (e.g. removal of dashes, commas, and suffixes such as ‘Inc’ and ‘LLC’) was performed to standardize chain identification. Chains with at least 15 locations (associated NPIs) or that dispensed > 1% of study prescriptions for a given drug were identified by the name listed in NPPES. All other chains were grouped together into an ‘other pharmacy’ category.

The outcome of interest was the manufacturer of the dispensed generic drug. The manufacturer for each prescription was identified by mapping the NDC on Medicare Part D claims to the manufacturer labeller name in the Medi-Span Master Drug Data Base (MDDB v2.5). Any references to ‘manufacturer’ in this paper refer to the manufacturer labeller name specified on a beneficiary’s Part D claim. This often corresponds to the name of the drug manufacturer that originally obtained approval for a given generic drug; however, there are instances where multiple labellers and distributors correspond to the same approved drug application.

Statistical analysis

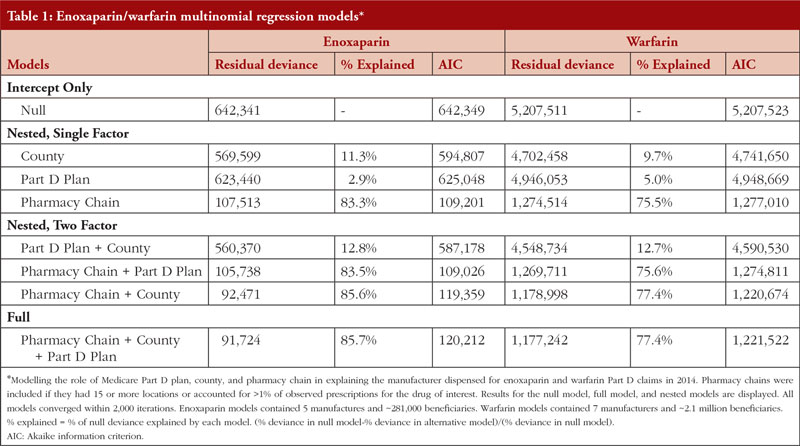

Separate multinomial logistic regression models were fitted for warfarin and enoxaparin. Generics manufacturer was the dependent variable (outcome) and pharmacy chain, county, and Part D Plan provider were predictors (factors). Beneficiaries were only counted once for each unique combination of exposure, factors, and outcome that was present. Small manufacturers (< 100 beneficiaries) and ‘other pharmacies’ (< 15 locations and = 1% of the study claims) were excluded from the model due to limitations of the data. Residual deviances were computed for full models as well as for nested models to depict variance explained by pharmacy chain, county and Part D provider. The Akaike information criterion (AIC) is provided for comparison of the different models. A smaller AIC suggests a relatively higher quality model.

Descriptive statistics were also created for the larger group of generic cardiovascular drugs described above. The distribution of manufacturers for each drug among prescriptions filled at a single pharmacy chain was summarized separately for CVS and Walgreens, the two pharmacy chains with the largest volume of prescriptions in the US.

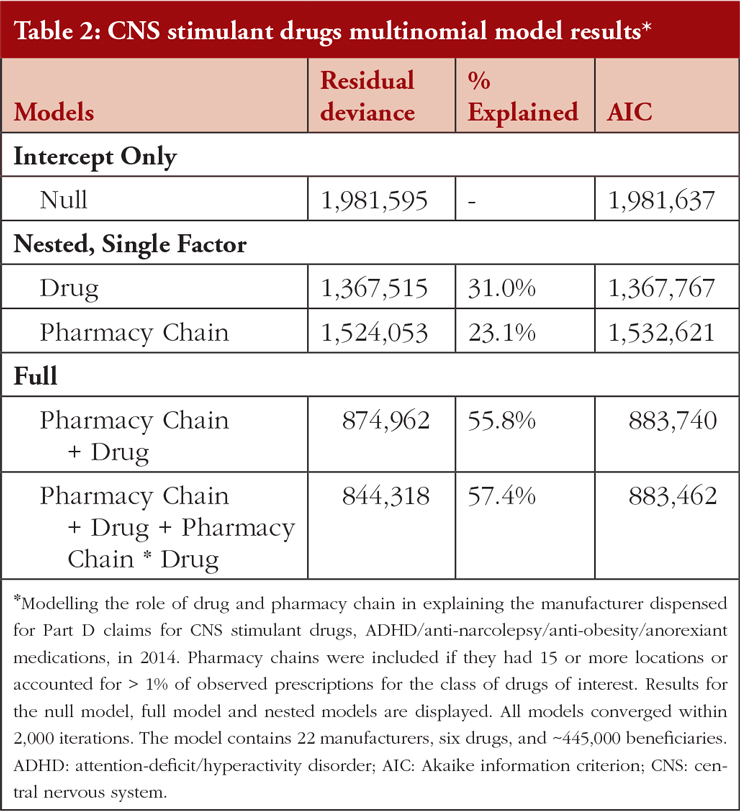

A single multinomial logistic regression model was fitted for CNS stimulant drugs. This analysis focused on pharmacy chain, as its importance had already been established. Thus, drug and pharmacy chain served as predictors and generics manufacturer remained the dependent variable (outcome). Beneficiaries were counted once for each unique drug-chain-manufacturer combination that was present. Again, small manufacturers and ‘other’ pharmacies were excluded. Residual deviance and AIC were calculated as before. Detailed descriptive statistics for data contained in each multinomial model can be found in Appendix B.

All analyses were conducted using SAS 9.4 (SAS Institute, Cary, NC, United States) and R 3.4.3 (R Foundation for Statistical Computing, Vienna, Austria).

Pharmacy chain is an important predictor of generics manufacturer choice for both enoxaparin and warfarin

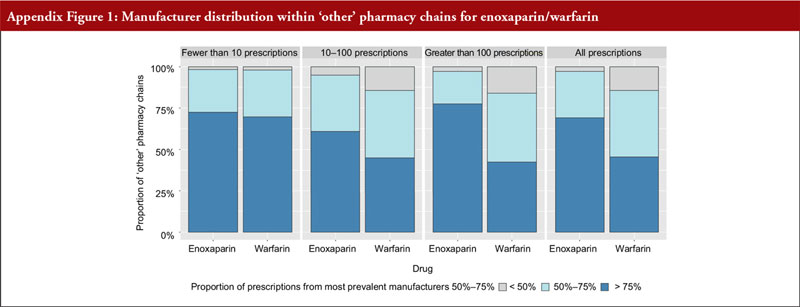

Pharmacy chain alone predicted over 75% of the variability in warfarin manufacturer and 83% of the variability in enoxaparin manufacturer, see Table 1. Including location by county or provider Part D plan in the model had a limited effect on per cent deviance explained. Among the small or independent pharmacies excluded from the regression analysis, descriptive statistics showed a similar association between manufacturer and pharmacy; 46% and 69% of these pharmacies dispensed over three quarters of their warfarin and enoxaparin prescriptions respectively from a single manufacturer, see Appendix Figure 1.

Specific patterns of generic drug manufacturers at individual pharmacy chains

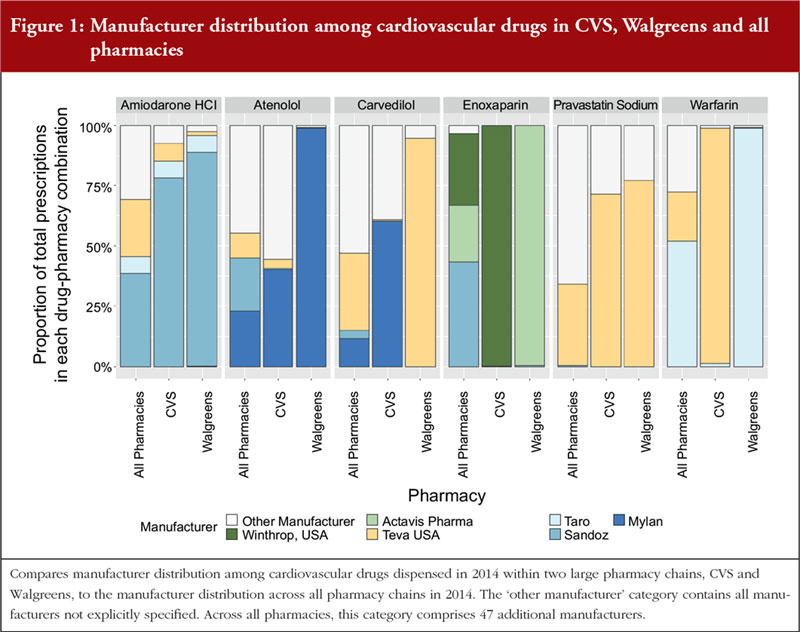

To illustrate specific pharmacy chain patterns of generics manufacturer use, several drugs that would be concurrently prescribed to patients with cardiovascular disease (including enoxaparin and warfarin) were evaluated together. The pattern of generics manufacturers for these products in two large volume pharmacy chains, Walgreens and CVS, is shown in Figure 1. If a Part D beneficiary filled enoxaparin and warfarin prescriptions at a Walgreens pharmacy in 2014, they had a 99% likelihood of receiving Actavis enoxaparin and a 99% likelihood of receiving Taro warfarin. If a beneficiary instead filled those prescriptions at a CVS, they would almost certainly receive Winthrop enoxaparin and would have a 98% likelihood of getting Teva warfarin. If that same beneficiary also filled a prescription for carvedilol at CVS, they would have had no chance of getting Teva carvedilol; however, at Walgreens, they would have had a high likelihood of getting Teva carvedilol. This demonstrates that pharmacy chain association with generics manufacturer can drive non-random associations between the manufacturers of multiple drugs. These pharmacy chain-manufacturer associa-tions can differ for different drugs; pharmacy chains do not necessarily contract all their cardiovascular drugs from a single manufacturer, even if both drugs are available from one manufacturer.

Duration of the associations between generic drug manufac-turers and pharmacy chains

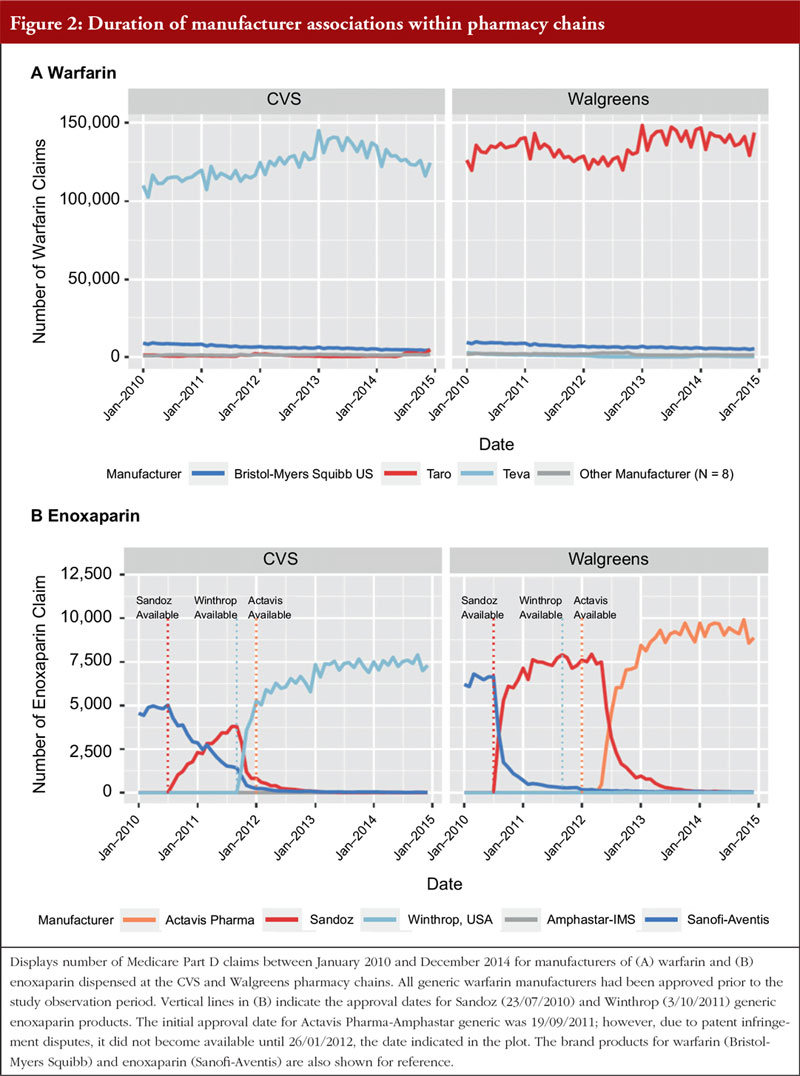

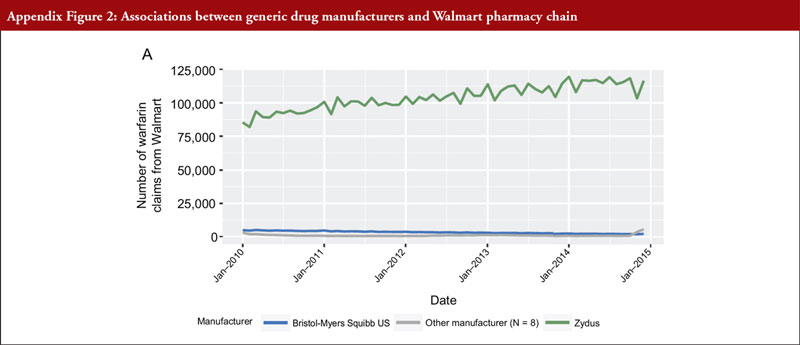

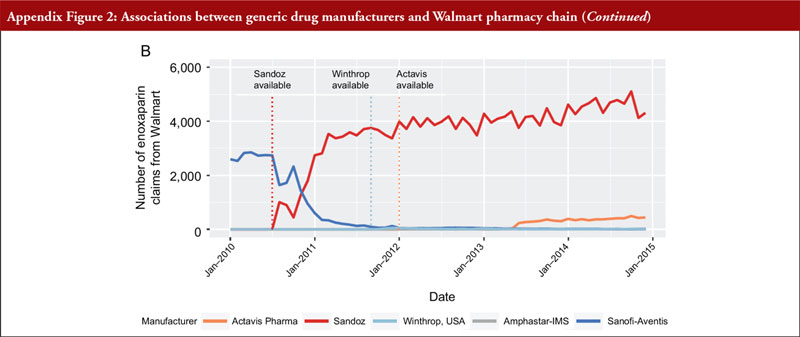

Although relationships between pharmacy chain and generic drug manufacturers are discernible over the course of a year, it is of interest to understand the duration of pharmacy chain-manufacturer associations over a longer time frame. The patterns of warfarin manufacturers dispensed over a five-year timeframe in two large volume pharmacy chains, CVS and Walgreens, are shown in Figure 2A. Teva is the predominant manufacturer for CVS, while Taro is the primary manufacturer dispensed by Walgreens. There is a relatively small amount of brand product (Bristol-Myers Squibb Coumadin) dispensed, but almost no other generic warfarin distributed over the entire five years for either pharmacy. This shows manufacturer-pharmacy chain associations can persist over extended periods and affect the specific generic drug patients receive. Figure 2B illustrates the manufacturer pattern over a 5-year time frame for CVS- and Walgreens-dispensed enoxaparin. CVS and Walgreens both dispensed the brand product (Sanofi-Aventis Lovenox) for the first seven months of the observed time-period before replacing it with the newly approved Sandoz generic enoxaparin. Sandoz was the primary generic drug dispensed at CVS for one year before being replaced by Winthrop enoxaparin for the rest of the observation period. In contrast, Walgreens dispensed Sandoz for 1.5 years before switching to Actavis enoxaparin. Appendix Figure 2 contains a similar analysis for warfarin and enoxaparin dispensed at Walmart.

Pharmacy chain is an important predictor of generics manufacturer choice for other multisource drugs

To explore manufacturer choice for other generic drugs, we fit a single multinomial regression model to eva-luate pharmacy chain-manufacturer relationships among CNS stimulant medications. Model results showed that, when both pharmacy chain and drug name were included in the model, over 55% of the variability was explained, see Table 2. Thus, the pharmacy that fills a patient’s prescription can affect the generics manufacturer received by the patient for other classes of drugs in addition to cardiovascular medications.

Our regression models demonstrated that pharmacy chain was the most influential factor in predicting the manufacturer of a prescribed generic drug. Within large pharmacies, pharmacy chain accounted for greater than 75% of the generics manufacturer associations for dispensed warfarin and enoxaparin, see Table 1. Associations between pharmacy chains and manufacturers persist over time, see Figure 2 and are also observed in smaller pharmacy chains, see Appendix Figure 1. Additionally, these associations occur in generics with different indications, as illustrated for generic cardiovascular drugs, see Figure 1 and generic CNS stimulant drugs, see Table 2.

Medicare Part D plan was not nearly as important as pharmacy chain in explaining the generics manufacturer dispensed, see Table 1. This result suggests that insurers are not the major driver of generics manufacturer choice. Furthermore, it suggests that the observed manufacturer-pharmacy chain association may extend to the broader health insurance market. The association between the location of beneficiaries and generics manufacturer was also relatively limited, suggesting that regional wholesale contracts or location-based demographics are lesser drivers of generics manufacturer choice. Thus, pharmacy chain contracts appear to be key drivers of generics manufacturer selection. As pharmacy chains are associated with different manufacturers for different drugs, our results suggest that contracts may not occur at the manufacturer level but at a third-party level such as a wholesaler.

These observations have strong economic implications for generics competition [15, 16] and its role in reducing drug prices and expanding consumer choice. The continual consolidation of wholesalers and pharmacy chains has resulted in a decrease in the number of distinct entities to which generic drug manufacturers can sell their products. This is expected to reduce generics competition and limit consumer choice. The striking division of the generics market by pharmacy chain may be driven by a variety of factors. One potential driver is generics manufacturer price, although its exact role is unclear. Public data [17] is available that summarizes average spending on generics by insurers and beneficiaries; however, this data may not directly correlate with the price paid by pharmacies.

If the dramatic differences in manufacturer choice are driven by price-based decisions, manufacturers are incentivized to reduce their prices to remain competitive. In the short term, continued consolidation may further reduce prices by increasing the bargaining power of wholesalers and pharmacy chains. However, as prices continue to drop, margins may be so reduced that some manufacturers are forced to exit the market, reducing consumer choice. Other manufacturers may decrease investments that would better assure drug availability to preserve profitability. In the long term, these outcomes might contribute to drug shortages and the price increases that accompany them [18].

Research comparing drug manufacturers [5, 6] is likely to continue, and the associations between generics manufacturers and pharmacy chains may impact epidemiological studies on generic drugs. Pharmacy chains may differ in the services they provide and in the populations they serve, see Appendix Table 1, in addition to the patterns of drug manufacturers they dispense. These differences could impact outcomes and confound studies if appropriate mitigations are not in place.

This study demonstrates that pharmacy chains are a key driver of generics manufacturer choice in the US. This impacts models of generic drug competition and may inform the design of epidemiologic studies on generic drugs. Further research on the role of pharmacy chains in the drug ecosystem is critical.

Competing interests: This manuscript reflects the views of the authors and should not be construed to represent FDA’s or CMS’s views or policies. We thank Drs Steven T Bird, PhD, PharmD, MS, and David J Graham, MD, MPH of the Office of Surveillance and Epidemiology, Center for Drug Evaluation and Research, US FDA for valuable input and comments. We thank Brad Lufkin, MPA, MSES, and Yoganand Chillarige, MPA, of Acumen, LLC for their contributions to manuscript editing and figure revisions.

Provenance and peer review: Not commissioned; externally peer reviewed.

1Office of Biotechnology Products, Office of Pharmaceutical Quality, Center for Drug Evaluation and Research, US Food and Drug Administration, Room 2230, White Oak Building 71, 10903 New Hampshire Ave, Silver Spring, MD 20993, USA

2Acumen, LLC, Burlingame, California, USA

3Office of Program and Strategic Analysis, Office of Strategic Programs, Center for Drug Evaluation and Research, US Food and Drug Administration, Maryland, USA

4Stanford University, Palo Alto, California, USA

5Centers for Medicare and Medicaid Services, Washington, DC, Washington, District of Colombia, USA

References

1. Association of Accessible Medicines. 2017 Generic Drug Access and Savings in the U.S. Report. 2017 [homepage on the Internet]. [cited 2019 Sep 7]. Available from: https://accessiblemeds.org/resources/blog/2017-generic-drug-access-and-savings-us-report

2. Greene JA. Generic: The unbranding of modern medicine. Baltimore, MD: Johns Hopkins University Press; 2014.

3. Gottlieb S. FDA working to lift barriers to generic drug competition. FDA Voice; 2017 [homepage on the Internet]. [cited 2019 Sep 7]. Available from: https://www.fda.gov/news-events/fda-voices-perspectives-fda-leadership-and-experts/fda-working-lift-barriers-generic-drug-competition

4. Kaiser Family Foundation. Follow the pill: understanding the U.S. commercial pharmaceutical supply chain. 2005 [homepage on the Internet]. [cited 2019 Sep 7]. Available from: https://kaiserfamilyfoundation.files.wordpress.com/2013/01/follow-the-pill-understanding-the-u-s-commercial-pharmaceutical-supply-chain-report.pdf

5. Kesselheim AS, Misono AS, Lee JL, Stedman MR, Brookhart MA, Choudhry NK, et al. Clinical equivalence of generic and brand-name drugs used in cardiovascular disease: a systematic review and meta-analysis. JAMA. 2008;300(21):2514-26.

6. Manzoli L, Flacco ME, Boccia S, D’Andrea E, Panic N, Marzuillo C, et al. Generic versus brand-name drugs used in cardiovascular diseases. Eur J Epidemiol. 2016;31(4):351-68.

7. Meredith P. Bioequivalence and other unresolved issues in generic drug substitution. Clin Ther. 2003;25(11):2875-90.

8. Al-Jazairi AS, Bhareth S, Eqtefan IS, Al-Suwayeh SA. Brand and generic medications: are they interchangeable? Ann Saudi Med. 2008;28(1):33-41.

9. Woodcock J, Khan M, Yu LX. Withdrawal of generic budeprion for nonbioequivalence. N Engl J Med. 2012;367(26):2463-5.

10. Flacco ME, Manzoli L, Boccia S, Puggina A, Rosso A, Marzuillo C, et al. Registered randomized trials comparing generic and brand-name drugs: a survey. Mayo Clin Proc. 2016;91(8):1021-34.

11. Eberhart MG, Yehia BR, Hillier A, Voytek CD, Fiore DJ, Blank M, et al. Individual and community factors associated with geographic clusters of poor HIV care retention and poor viral suppression. J Acquir Immune Defic Syndr. 2015;69 Suppl 1:S37-43.

12. Amstislavski P, Matthews A, Sheffield S, Maroko AR, Weedon J. Medication deserts: survey of neighborhood disparities in availability of prescription medications. Int J Health Geogr. 2012;11:48.

13. Brooks JM, Doucette WR, Wan S, Klepser DG. Retail pharmacy market structure and performance. Inquiry. 2008;45(1):75-88.

14. Polinski JM, Brookhart MA, Glynn RJ, Schneeweiss S. Medicare part D’s impact on antipsychotic drug use and costs among elderly patients without prior drug insurance. J Clin Psychopharmacol. 2012;32(1):3-10.

15. Berndt ER, Aitken ML. Brand loyalty, generic entry and price competition in pharmaceuticals in the quarter century after the 1984 Waxman-Hatch Legislation. Int J Econ Bus. 2011;18(2):177-201.

16. National Bureau of Economic Research. Berndt ER, Newhouse JP. Pricing and reimbursement in U.S. pharmaceutical markets [homepage on the Internet]. [cited 2019 Sep 7]. Available from: http://www.nber.org/papers/w16297

17. Centers for Medicare & Medicaid Services. Medicare Part D drug spending dashboard & data (enoxaparin and warfarin manufacturer average spending per dosage unit). 2014 [homepage on the Internet]. [cited 2019 Sep 7]. Available from: https://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/Information-on-Prescription-Drugs/MedicarePartD.html

18. Dave CV, Pawar A, Fox ER, Brill G, Kesselheim AS. Predictors of drug shortages and association with generic drug prices: a retrospective cohort study. Value Health. 2018;21(11):1286-90.

Multisource generic drugs were classified using the Generic Product Identifier code at level 4 (GPI4), the level of the drug name. This identifier groups together all manufacturers of a generic drug. The GPI4 for warfarin (warfarin sodium) is 8320003020 and for enoxaparin (enoxaparin sodium) is 8310102010. For a description of pharmacy chain generic brand patterns, the following cardiovascular drugs (GPI4) were studied in addition to warfarin and enoxaparin: carvedilol (3330000700), pravastatin sodium (3940006510), atenolol (3320002000), and amiodarone HCl (3540000500). The criteria for selection included the following: produced by at least three of the same manufacturers found to produce warfarin and/or enoxaparin; found on at least one million Part D claims.

Medications prescribed for the treatment of ADHD, narcolepsy, obesity, and anorexia (GPI level 1 category #61) with more than one manufacturer were also evaluated. These included CNS stimulants with the following generic drug product names (GPI4 codes): amphetamine-dextroamphetamine (6110990210), dexmethylphenidate HCl (6140001610), dextroamphetamine sulfate (6110002010), methylphenidate HCl (6140002010), modafinil (6140002400), and phentermine HCl (6120007010).

Three multinomial regression models were run in this study: one for warfarin, one for enoxaparin, and one for central nervous system (CNS) stimulants (GPI level 1 #61). The number of generic drug manufacturers, pharmacy chains, Part D plans, counties and beneficiaries included in each model, where relevant, are displayed below. Breakdowns are also provided for all six drugs contained within the single CNS stimulant medication model for context. Cells that are missing information represent variables not included in the specified model. Note that all drugs modelled had at least two generic manufacturers. All manufacturers in a given model were dispensed to at least 100 beneficiaries. All models were run on larger pharmacy chains, i.e. chains with at least 15 locations or chains that made up > 1% of the Part D claims for the drug or class of drugs modelled.

In order to evaluate trends in smaller pharmacies, descriptive statistics were created to summarize manufacturer distribution among warfarin and enoxaparin prescriptions filled by pharmacies grouped into the ‘other’ pharmacy category. The percentage of these pharmacies that had > 75%, 50%-75%, or < 50% of their dispensed 2014 warfarin or enoxaparin prescriptions originating from a single manufacturer was compiled, stratified by size of chain. ‘Other’ pharmacy chains were defined as having fewer than 15 locations and less than or equal to 1% of observed prescriptions for the drug of interest. Chain size is approximated by number of warfarin or enoxaparin prescriptions dispensed. For enoxaparin, 14,398 chains fell into the ‘other’ category, of which 9,690 had = 10 prescriptions, 4,275 had 11-100 prescriptions, and 433 had > 100 prescriptions. For warfarin, 19,475 chains fell into the ‘other’ category, of which 1,634 had = 10 prescriptions, 7,021 had 11-100 prescriptions, and 10,820 had > 100 prescriptions.

Part D claims between January 2010 and December 2014 for manufacturers of: (A) warfarin, and (B) enoxaparin, dispensed at the Walmart pharmacy chain. All generic warfarin manufacturers had been approved prior to the study observation period. Vertical lines in (B) indicate the approval dates for Sandoz (23/07/2010) and Winthrop (3/10/2011) generic enoxaparin products. The initial approval date for Actavis Pharma-Amphastar generic was 19/09/2011; however, due to patent infringement disputes, it did not become available until 26/01/2012, the date indicated in the plot. The brand products for warfarin (Bristol-Myers Squibb) and enoxaparin (Sanofi-Aventis) are also shown for reference.

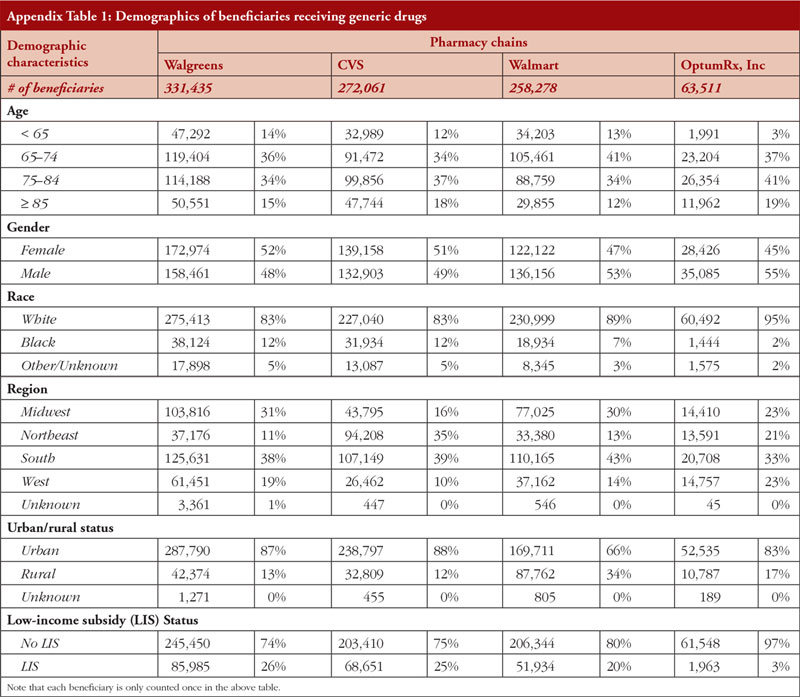

The relationship between multisource manufacturers and pharmacy chains may impact outcomes in ways besides manufacturer-manufacturer associations. The populations that use different pharmacy chains can differ. To evaluate this, we compared demographics of Part D beneficiaries receiving warfarin across four retail pharmacy chains with some of the largest percentages of beneficiaries with Part D claims for warfarin in 2014. Each beneficiary was assigned to a single pharmacy chain. For instances, where a beneficiary had claims originating from multiple pharmacy chains, the beneficiary was assigned to the pharmacy that corresponded to the majority of their claims. In cases where the beneficiary had the same number of claims with two or more pharmacies, they were assigned to the pharmacy chain that corresponded to the earliest claim date. A beneficiary’s low-income subsidy (LIS) status was assigned based on their status at the time of their first 2014 claim. A beneficiary’s urban/rural status was determined based on the beneficiary’s county of residence at the time of their first 2014 claim.

OptumRx, Inc had an older population that was less likely to receive LISs and Walmart had a larger rural population relative to the other pharmacy chains. Region also varied across pharmacies. Each pharmacy chain has a distinct client profile. It is clear that differences in characteristics such as age, geographical location, and socioeconomic status exist across pharmacy chain populations, and must be controlled for in studies comparing multisource products.

|

Author for correspondence: Steven Kozlowski, MD, Office of Biotechnology Products, Office of Pharmaceutical Quality, Center for Drug Evaluation and Research, US Food and Drug Administration, Room 2230, White Oak Building 71, 10903 New Hampshire Avenue, Silver Spring, MD 20993, USA |

Disclosure of Conflict of Interest Statement is available upon request.

Copyright © 2019 Pro Pharma Communications International

Permission granted to reproduce for personal and non-commercial use only. All other reproduction, copy or reprinting of all or part of any ‘Content’ found on this website is strictly prohibited without the prior consent of the publisher. Contact the publisher to obtain permission before redistributing.

Source URL: https://gabi-journal.net/pharmacy-chain-drives-choice-among-manufacturers-of-generic-drugs-in-the-us-medicare-population.html

Copyright ©2024 GaBI Journal unless otherwise noted.