Author byline as per print journal: Ljiljana Sović Brkičić, MPharm; Brian Godman, BSc, PhD; Martina Bogut, BSc; Miron Sršen, MD; Hye-Young Kwon, BPharm, MPH, PhD; Winnie de Bruyn, BSc; Tonko Tabain, MD

|

Introduction: Croatia has introduced a number of reforms to contain pharmaceutical expenditure whilst increasing access to new medicines. These include new regulations and new ordinances in 2013 including the pricing of new medicines and lowering the price of generics. |

Submitted: 19 January 2015; Revised: 24 April 2015; Accepted: 27 April 2015; Published online first: 11 May 2015

Rising pharmaceutical expenditure is causing concern among countries, with expenditure rising by more than 50% in real terms during the past decade among OECD countries [1, 2]. These concerns have resulted in multiple reforms and initiatives across Europe, which includes regulations regarding prices, reimbursement and utilization of medicines [2, 3]. Initiatives for established medicines include measures to obtain low prices for generics as well as encourage their prescribing [3–9]. This includes both internal reference pricing (IRP) systems and external reference pricing (ERP) [9–13], with IRP currently utilized among 20 or more EU Member States and ERP among 24 EU Member States [9, 12]. Croatia is no different and has introduced a number of reforms in recent years to reduce debt levels, add new medicines to the reimbursement list and improve the quality of care [14–17]. Measures include restricting medicines to second line, with follow-up by physicians working for the Croatian Health Insurance Fund (CHIF) if abuse is suspected [18], as well as strict control of pharmaceutical company activities, with adherence enhanced through financial penalties [14, 15]. In addition, regulations for lowering the prices of successive generics for a given molecule are in place [14, 18].

However, there is a continual need to conserve resources, as well as a continuing need to encourage the reimbursement of new valued medicines, given the level of unmet need, ageing populations and continued high unemployment affecting CHIF revenues [19, 20]. This led to the development of a new ordinance for the pricing of both new and established medicines including biosimilars. The old ordinance was published in the Official Gazette 155/2009, and its amendment published in the Official Gazette 22/2010, while the new ordinance was published in the Official Gazette 83/2013 and its amendment in the Official Gazette 12/2014 and Official Gazette 69/2014 [19–24]. There is a recognized need to evaluate the influence of the new ordinances on potential savings, and use the findings to plan further pertinent measures.

The ordinance establishing the criteria for the inclusion of medicinal products onto the basic and supplementary Reimbursement Lists of the CHIF has been enacted since 2013 (Official Gazette 83/2013) [20]. The decision on accepting or rejecting new medicines for reimbursement is undertaken by the Committee for Drugs and Medicinal Products within the Administrative Council of the CHIF following a recommendation by the Commission for Drugs, which consists of 13 members who are all experts in their specific disease area.

Key criteria for assessing the value of new medicines in Croatia, and their potential prices, include improved outcomes versus current standards including improved quality of life and/or reduced adverse effects, more ‘user-friendly’ formulations improving compliance as well as improved overall efficiency [14, 15]. In addition, whether this is a medicine where no treatment has previously existed; alternatively, a replacement treatment. There is also the potential for price reductions or price: volume agreements, including pay-backs or cross-product agreements, for new active substances with budget impact analyses requested for new medicines based on best practice and defined by the ordinance [14, 15, 17, 20].

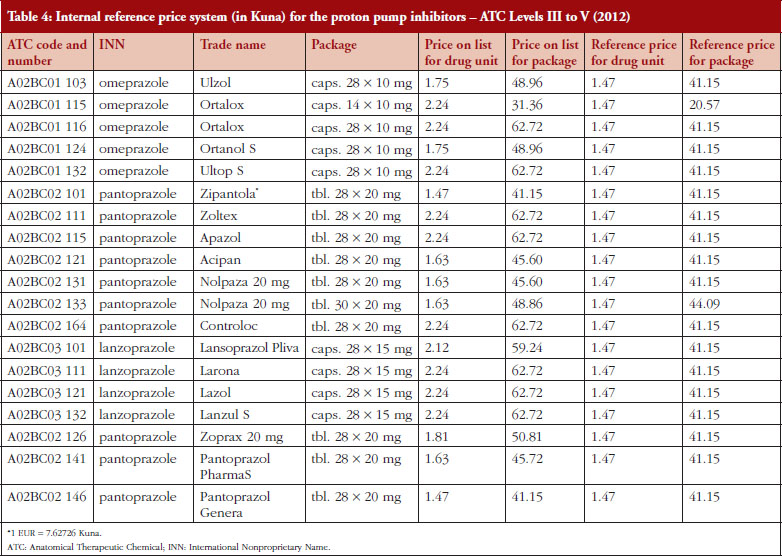

The prices of established as well as new medicines are regulated by ordinances including biosimilars, vaccines and small molecules [19, 20]. The ordinances also describe the procedure of calculating annual drug pricing (external reference pricing, ERP) as well as the method for setting reference prices of medicines and reference price systems (internal reference pricing, IRP). ERP is a process in which the prices of medicines are compared with prices of medicines in comparable countries (example contained in Table 3). IRP is based on the Anatomical Therapeutic Chemical (ATC) classification. This can be at ATC Level III (pharmacologic group, e.g. lipid modifying agents), Level IV (pharmacologic class, e.g. HMG CoA reductase inhibitors) or Level V (individual molecule) [14, 17, 25]. IRP is a process in which CHIF established the reference prices of medicines, which are the reimbursed prices (Example contained in Table 4). CHIF covers the reference price, with patients covering any additional costs themselves for a more expensive product out-of-pocket.

The reimbursed price on the two lists (basic and supplementary) is the ex-factory price combined with wholesale margins and other taxes up to 8.5%, which is wholesale price (WP) and tax (VAT) at 5%, as well as a pharmacy mark-up (fee) which is constant per package of medicines. Prices for non-reimbursed medicines including over-the-counter medicines are typically determined by market demand. Prices include WP, taxes (5% and 25%) and pharmaceutical margins (up to 35%).

The ordinances conform to the Directives of the European Commission regarding the pricing of medicines. According to these directives, each country determines the price of their medicines on the basis of a self-selected model, which must be clear and transparent, and must be implemented within set deadlines and in compliance with the directives [26]. The basic list of drugs, which are fully reimbursed, and the supplementary list of drugs, with CHIF covering the reimbursed part with the patient covering the remainder, are the final results of the current procedures in 2013 [27, 28]. The basic list also includes expensive medicines that are funded out of different budgets. Drug lists are constantly changing as new drugs are included, indications are revised and established medicines removed [27–29].

In Croatia, the share of public expenditures for health care is currently 6.6% of GDP [30, 31], with 14.6% spent on pharmaceuticals in 2012 [31]. This is down from 17% in 2007 [31]. The various reforms in recent years have resulted in similar financial expenditure on prescription medicines in 2012 compared with 2008, i.e. Kunas 3,303 billion in 2012 (Euros 433 million) versus Kunas 3,392 billion (Euros 445 million) in 2008. In addition between 2009 and 2011, 85 new medicines were added to the reimbursement list [30]. Overall, 3,044 packages of medicines were included in the basic drug list in 2012 and 390 drugs on supplementary list. This compares with 2,047 packages of medicines in the basic list and 262 in the supplementary list in 2008.

The objectives of this paper are to: 1) report on the new ordinances including changes in the reference price systems and compare these with the previous ordinances; 2) compare potential savings from the changes in the reference price system (internal reference pricing, IRP) at ATC Level III to V (current system) to just ATC Level V for comparative purposes among the 54 current reference price groups as a result of the recent reforms; 3) suggest additional measures for consideration by CHIF in the future as CHIF strives to continue to provide comprehensive and equitable healthcare.

We are not aware of many publications that have assessed the impact of changes to their ERP and IRP systems, although authors have calculated potential savings through converging prices to the average [12]. Consequently, we hope the findings and their implications will be of interest to the authorities in Croatia as well as other European countries that use reference pricing systems since we are aware there are some concerns with reference pricing initiatives [10, 17]. We will discuss these in the context of the findings in Croatia to stimulate further debate in this growing area of interest.

This includes a narrative review of the reforms comparing the old ordinances (2009) with the new ordinances (2013) among the co-authors (principally LSB), including the regulations surrounding:

a. Placing new medicines on the list either as replacements for existing established medicines or entirely new treatments where none have existed before. This will be compared and contrasted with the old ordinance.

b. Placing new generic medicines onto the drug lists, as well as comparing the old and new ordinances.

c. The model for calculating the ERP for medicines and the implications, see Table 3.

d. Internal pricing using a reference price system. We will describe the model of the IRP as well as the projected potential savings based on expenditure of medicines in the various reference price groups in 2012, see Table 4.

For ERP, this included comparing potential savings with the old and new ordinances.

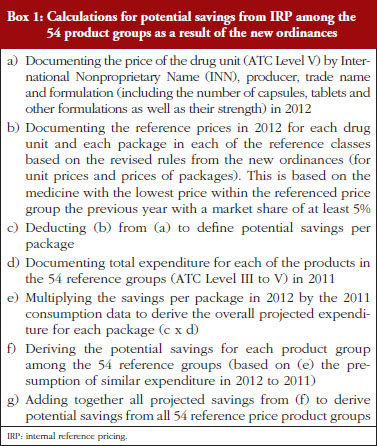

The calculations of potential savings from the changes in the IRP system for the 54 product groups are included in Box 1.

The potential savings arising from all the changes in the ordinances will also be calculated to provide a basis for any pertinent additional future reforms. The analytic methods applied in the various situations are descriptive epidemiological methods, primarily involving a comparative analysis of pricing models of medicines under the old and new ordinances.

The quality of the data is assured by regular auditing of the CHIF database.

Suggestions for potential additional measures and reforms that CHIF could consider introducing in the future will be based on the considerable experience of the co-authors working with health authorities from different countries in analysing health reform policies.

This will be divided into four sections starting with placing new medicines placed onto the reimbursed list including new generics.

A. Pricing of new medicines or new treatments including new generics

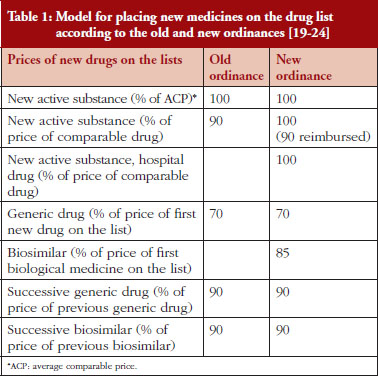

The principal difference between the old and new ordinances is the pricing of biosimilars as well as new hospital medicines, see Table 1. Hospital medicines are now included where there is an added health benefit compared with existing standards as there have been problems with their pricing in the past in the implementation and finalization proceedings. The list price in the new ordinance for new active substances demonstrating additional health benefit versus existing standards is now increased to 100% of their calculated prices, up from 90% of the comparable medicine. There is a 10% patient copayment for ambulatory care medicines but not hospital medicines, see Table 1.

For new medicines or new active treatments where no treatment has existed before for the particular disease, the price is calculated based on ERP, see Table 2 as well as a % of the Average Comparable Price (ACP), see Table 1, based on prices of similar treatments in comparable countries, see Table 2.

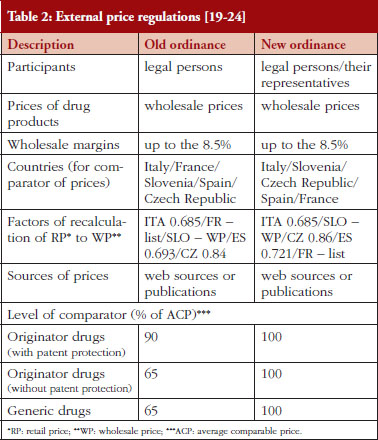

It is envisaged the order of the countries used for ERP, see Table 2, alongside changes from the factors relating to retail versus wholesale prices, will affect subsequent reimbursed prices for new medicines in Croatia. This is because the average price of the package of medicines in comparable countries (without tax and margins) is translated into the unit price (in Kunas) for that country and then into the price of the package of the drug that will be available in Croatia. After the translation, the ACP of the drug is calculated. The ACP is calculated as the average price of the same drug (same generic name, and the same or similar form and packaging) in the three chosen countries starting with Italy, Slovenia and Czech Republic, according to the new order established by the ordinance, see Table 2. In cases where there is no comparative price for the new medicine in one country, then the average price of the medicine from the next country in the list of chosen countries is included and so on, see Table 2.

As seen in Table 1, the price calculations for the first and subsequent generics for small molecules are similar between the old and new ordinances. The main difference is that biosimilars are now included to address this anomaly, with the price of the first biosimilar at 85% of the originator price. The inclusion of biosimilars should accelerate savings as more biosimilars are launched for existing molecules and more biologicals lose their patents given the current high prices for biological medicines [32–38].

B. Pricing of medicines under external reference pricing

The principal differences in the ordinances for the ERP of existing medicines and new medicines where no medicine has existed before is the order of the reference price countries for calculating external reference prices, see Table 2.

ERP of established medicines is carried out once a year to make sure that the prices of established medicines in Croatia are not higher than the chosen European countries. ERP for established medicines used to take place the first Monday in February each year [20], but will now take place on the first Monday in March [21]. If the price of the medicine in Croatia is found to be higher than the ACP price, its price is subsequently reduced to the level of the ACP.

The sources for external pricing data are similar, i.e. official data from the countries included in the ordinances, however, there is now greater reliance on web sources than publications, see Table 2. Data sources include:

• Old ordinance: Italy – Informatore Farmaceutico; France – Vidal; Slovenia – Register; Spain – Catalogo de Medicamentos; Czech Republic – www.vzp.cz

• New ordinance: Italy – www.Codifa.it; Slovenia – http://www.jazmp.si; Czech Republic – http://www.sukl.cz/; Spain – Catalogo de Medicamentos: latest electronic version; France – Vidal Expert: latest electronic version

Other changes include greater interaction with the legal persons and their representatives in each country, which are involved in the registration and/or pricing of medicines during the reference pricing process.

There have also been changes to some of the factors for the recalculation from retail to wholesale prices to remove taxes and margins from the included countries and to enable comparisons based on WPs. The presented factors for the recalculation of the reference prices for the comparable countries, published table as a part of the ordinances, are included in Table 2.

Under the new ordinances, prices remain at 100% of the ACP of the medicine under the various regulations for new and established medicines including generics and biosimilars, see Tables 1 and 2. Consequently, the calculation of the prices of both new and established medicines under the new ordinance appears applicable and acceptable to all key stakeholder groups. This was not the case with the old ordinances, especially if Croatia was a reference price country, as under the old ordinance prices were reduced by 10% and 35% of the ACP, i.e. prices were at 90% if patent protected and 65% if no patent protection of the ACP, see Table 2. Having said this, the order of countries for ERP has changed potentially impacting on prices in Croatia along with changes in the factors involved, see Table 2. In addition, the wording of the ordinances has changed, see Table 2. 100% under the new ordinances for both originator and generic products enables fair market competition based on ACPs.

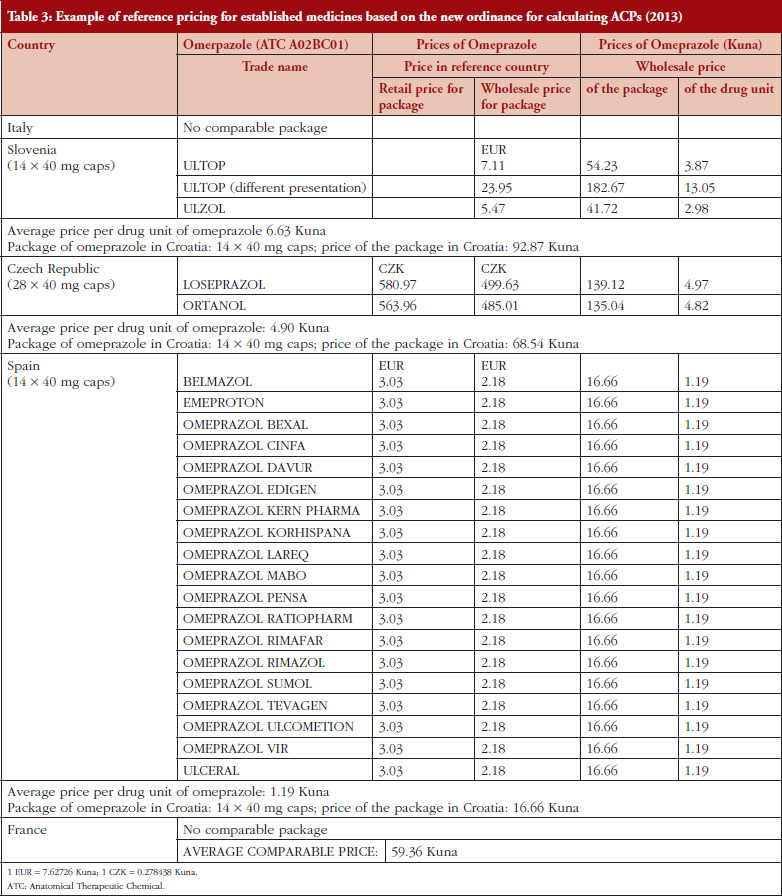

Table 3 provides an example of the impact of the change in the ERP policy for omeprazole, with the change in the factors for calculating ACPs based on the change in factors from retail to wholesale prices as well as changes in the order of the countries, see Table 2.

C. Internal reference pricing system

The internal reference pricing system (IRP) has been introduced since it can happen on the reimbursed list that there are the same medicines with different prices. This is because new medicines can be placed on the list which contain the same INN, same dosage and packaging but with different prices due for instance to successive generics necessarily being priced 10% lower than the previous one for reimbursement, see Table 1. Similarly, new single-sourced products (ATC Level III to V) can be placed on the reimbursement list at potentially lower prices. Similar to ERP, IRP takes place once a year once ERP has been performed. If the prices of the same medicine differ, their prices are subsequently reduced to the level of the reference price or lower.

Prices of the originators are subsequently subject to IRP based on the lowest priced molecule in the class (ATC Level III to V) with a market share of 5% or more of the total market by volume. Should the authorization holder not accept the proposed price, i.e. want to keep the old price, the medicine is placed on the supplementary list with CHIF paying the reference price with patients covering any additional price themselves out-of-pocket.

To illustrate this, a comparison has been performed, see Table 4, building on the methodology described in Box 1. Reference prices are determined in relation to the unit price of the drug, or at the price of the package for the drug, or the amount of active compound in a unit form of the medicine based on similar defined daily doses (DDDs) [25]. We are aware the World Health Organization (WHO) does not recommend the use of DDDs to compare prices of medicines. However, we are not aware of another appropriate comparator for determining (comparison) of prices especially if dosage forms and pack sizes vary. Determining reference prices of medicines by ATC Level III to V helps ensure similar prices are paid for the same molecule as well as for medicines that have the same or similar therapeutic effect. The reference price of a medicine requiring a prescription is determined by searching for the medicine with the lowest price within the pertinent reference group, which in the previous year had a market share of at least 5% [14]. We are also aware the reimbursement list may contain medicines that have not achieved a market share of 5%; however, their price cannot be used as reference price.

The reference groups (currently 54) for IRP are determined by the Committee for Medicinal Products of the Ministry of Health. If the marketing authorization holder for the medicine, or its authorized representative, accepts the proposed reference price, their medicines will be placed on the basic list of drugs. As mentioned, if the authorization holder (originator or branded generic) rejects the proposed reference price, or keeps the old price, the medicine is placed on the supplementary list of medicines and the CHIF just pays the reference price for the particular medicine. Any difference in the price is subsequently paid by the patient out-of-pocket. The authorization holder (legal persons and their representatives) may also propose a price of their medicine that is lower than the current reference price to enhance its market share.

Table 4 provides an example of the model for the IRP system (ATC Level III to V) for the proton pump inhibitors (PPIs) in 2012.

D. Potential savings with the new ordinances

Calculations undertaken before the new ordinances were implemented regarding ERP believed the new ordinances, with changes in the order of the reference price countries, see Table 2, would lower prices by an average of 8% to 10%. This is less than the potential savings of 10% to 35% under the old ordinance with prices lowered by 65% to 90% of the ACP, see Table 2. However, the documented price reductions under the old ordinance were seen as large and potentially restrictive. The changes in the new ordinances to 100% of comparative prices, see Table 1, are seen as more acceptable to key stakeholder groups especially if Croatia is a reference priced country.

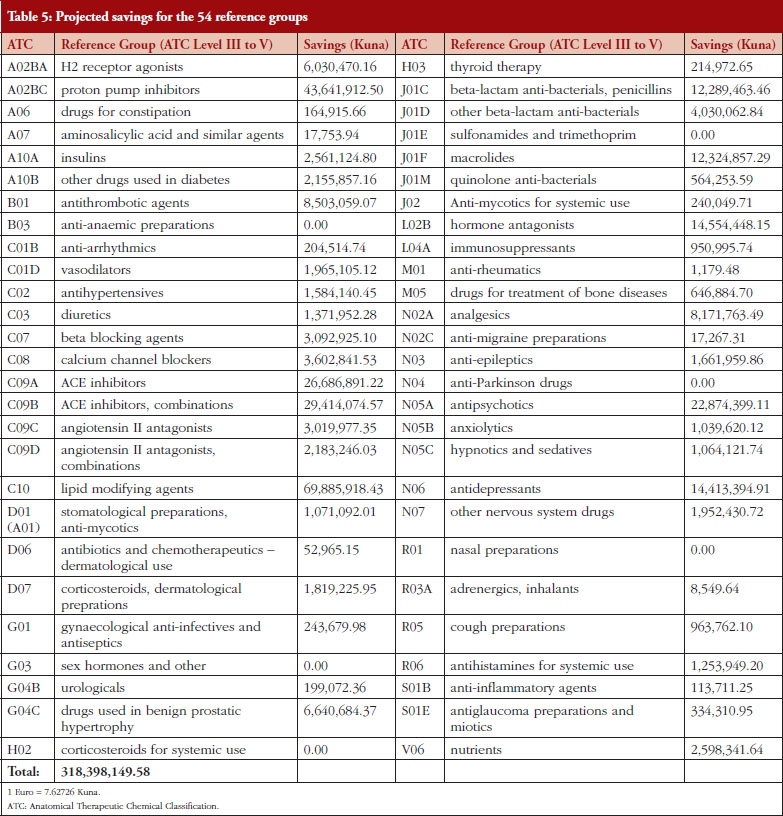

The overall projections for potential savings are based on changes in the ERP system with the new ordinances, incorporating all medicines in the basic and supplementary list including generics and biosimilars, factors concerned with wholesale and retail prices as well as changes in the order of the reference countries, see Tables 1 and 2, described in the Methodology section. This does not apply to new medicines where none has existed before to treat a given disease as these costs will be in addition. There are separate projections based on changes in the IRP system, including medicines placed in the 54 reference groups. As mentioned, IRP in Croatia is determined at ATC Level III to V. Consequently, this was the principal model used to calculate potential savings for the new ordinances in the current reference groups. Potential savings were compared to just concentrating at ATC Level V when determining potential IRP for comparative purposes.

Based on 2011 consumption and projected savings per package in 2012 outlined in the Methodology section, projections showed possible savings of Kunas 318.4 million for CHIF for the 54 reference groups, see Table 5. This represents savings of 9.64% for reimbursed drugs based on projected 2012 consumption figures. Setting the reference price of medicines (IRP) at the ATC Level V rather than III to V yielded potential savings of Kunas 254.45 million, i.e. 7.7% of total CHIF expenditure on ambulatory care medicines in 2012 [34]. Table 5 shows projected savings for each of the 54 reference groups (ATC Level III to V). 2,028 packages of different medicines were included in the 54 reference price groups in 2012, forming the basis of the calculated savings.

Projected savings from the new ordinances for CHIF for medicines on the current lists will grow as more generic medicines are launched as well as more biosimilars for the same medicine and for new biological medicines losing their patents.

Different European countries have used different models and approaches for determining the price of new and established medicines including generics. This includes both IRP and ERP, with differences in ERP in terms of the number of countries chosen, their sequence, methods for establishing reference prices as well as time frames for their review [10, 17, 39–42].

This paper demonstrates that changes in the reference pricing system can lead to considerable differences in overall reimbursed expenditure. There have been concerns that countries with small populations cannot obtain low prices for medicines [40]. However, this paper demonstrates that a European country with a smaller population, i.e. 4.27 million inhabitants in 2012 year, was active with introducing a variety of measures to help control pharmaceutical expenditure whilst increasing access to new medicines. This includes changes in reference price systems and the pricing of medicines losing their patent.

The calculated savings from the changes in the ERP system, including the order of chosen countries, see Table 2, were estimated at an average of 8% to 10%. The calculated savings from the changes in the IRP systems were estimated at Kunas 318.4 million among the 54 reference groups, see Table 5, i.e. 9.64% of reimbursed drug expenditure in 2012, reduced to Kunas 254.45 million, i.e. 7.7% of total CHIF expenditure, if the IRP is just based on ATC Level V [34]. These findings endorse CHIF’s decision to use ATC Level III to V rather than just ATC V for IRP in the new ordinances. This provides guidance to other countries using reference pricing particularly once generics become available in a class to help control pharmaceutical expenditure. This difference is also a potential way to address concerns regarding the lack of transparency in the prices of reference priced countries.

We are aware of a number of controversies surrounding ERP. This includes the fact that prices of medicines in countries may not reflect actual prices [10, 12, 43, 44]. In addition, pharmaceutical companies may preferentially launch their new medicines initially in traditionally higher price countries thereby potentially increasing the prices in the remaining countries that directly or indirectly reference them [12]. Thirdly, price reductions in one reference country may not automatically apply to other reference countries unless there are mechanisms to rapidly assess this. As a result, reduce potential savings [12]. Finally, pharmaceutical companies could potentially withhold launching their new medicines in lower priced countries as this may adversely affect overall profitability. However, the initial reforms in Croatia resulted in 85 new medicines being added to the reimbursement list between 2009 and 2011 coupled with a deficit reduction [14, 30]. This was up from 47 new medicines between July 2009 and 2010, with 13 new medicines added to the list of expensive hospital products [15]. In addition, we believe the changes in the new ordinance, see Tables 1 and 2, should be beneficial to all key stakeholder groups with prices of both patented and multiple sourced medicines remaining at 100% as opposed to 65% to 90% of ACP. Whilst potentially resulting in lower savings for CHIF, this should enhance the attractiveness of this ordinance to key stakeholder groups, addressing some of the concerns that companies will not launch their new medicines in lower priced countries. The new ordinances with no automatic price reductions for new medicines, see Tables 1 and 2, should also be beneficial to pharmaceutical companies enhancing their desire to launch new medicines in Croatia. As mentioned, lower prices for established medicines including generics and biosimilars should be beneficial to patients, reducing their copayment levels as well as creating headroom for new medicines.

We are also aware that there are controversies surrounding the selection of countries for ERP, although most countries appear to reference those of similar income levels [10]. In this respect, we believe the change in the order of countries brings Croatia in line with other European countries, i.e. higher income countries tend to include higher income countries in their basket whereas lower income countries tend to reference lower income countries [10]. The use of five countries is also similar to other European countries, who tend to have less than 10 countries in their reference baskets [10]. Wholesale prices should also be more uniform that pharmacy prices as there can be considerable differences in pharmacy remuneration and taxes between countries [10]. As a result, endorsing the new approach, see Tables 1 and 2.

We are aware that some European countries review their prices more regularly than Croatia to improve transparency [9, 11]. Applying this approach in Croatia could potentially lead to greater savings than those achieved by the recent changes in the ordinances, see Tables 1, 2, and 5. However, instigating a greater number of internal and external pricing reviews would need new procedures and workflows as well as consensus in how this can be achieved. In addition, an assessment of the implications for all key stakeholder groups including wholesalers, pharmacies, marketing authorization holders and others. Alongside this, the necessity to have transparent information systems that will continually monitor prices of medicines in the ERP countries as well as possible changes to legal entities. The increased costs would impact on the extent of any potential savings. Having said this, this possibility should not be discarded if further savings are needed in Croatia in the future.

Finally, we are aware that the new ordinance has not discussed potential initiatives to improve the quality of prescribing apart from prescribing restrictions for certain medicines, e.g. angiotensin receptor blockers and curbing pharmaceutical company marketing activities [14, 18]. In addition, the instigation of e-prescribing from January 2011 is making medicines more accessible without patients visiting their physician. Possible measures could include initiatives to reduce adverse drug reactions (ADRs) and drug interactions including decision support systems in conjunction with e-prescribing [45, 46]. Treating ADRs can be costly to health authorities as well as adversely affecting the health of patients. Published studies have shown that ADRs add to the costs of health care through increasing hospital admissions and other costs [47–49]. For example, the average treatment costs in Germany were estimated at approximately Euros 2,250/ADR, equating to Euros 434 million per year [50], with the cost of drug-related morbidity and mortality exceeding US$177.4 billion in the US in 2000 [51]. This is despite the proclaimed goal of the authorities in Croatia to introduce and implement for instance external evaluation of the quality of healthcare institutions [31].

The strength of these findings is based on the fact that the ordinances and findings are based on CHIF data, which is regularly audited. The weakness is the fact that these are projections. We will continue to monitor the situation and provide feedback to CHIF if further ordinances are needed.

Potential ways forward in addition to potential price cuts to help Croatia stay within agreed pharmaceutical expenditure [52] could include greater education of patients concerning the medicines they receive. As a result, reduce unnecessary requests for medicines as well as improve compliance, which is a concern in patients with chronic asymptomatic diseases [53, 54]. Other potential initiatives could include the instigation of active regional drugs and therapeutic committees deciding which medicines to use to treat common diseases in ambulatory care, building on the current reimbursement list. This is because there are concerns with the evidence base of the medicines included in the current reimbursement list [55], as well as typically physicians only knowing a relatively limited number of medicines well. This was the philosophy of the Stockholm Metropolitan Healthcare Region in Sweden where there has been a tradition of advocating ‘each recommended medicine should be of high value to the patient’ [56, 57]. Since 2000, approximately 200 medicines have been selected for common diseases in ambulatory care [56]. Respected specialists, working jointly with clinical pharmacologists, pharmacists and general practitioners in over 20 expert groups, suggest which medicines should be selected and included in the ‘Wise List’ [56, 58], which is then widely communicated and disseminated throughout Stockholm [56, 57]. Physician adherence to the voluntary ‘Wise List’ has increased during the past 10 years, now reaching 87% of all prescriptions, enhanced by physician trust in the ‘Wise List’ with its robust methodologies [56, 58].The ‘Wise List’ is now being translated into other languages to provide a stimulus to introducing such initiatives [59].

Concurrent with this, there is also likely to be increasing scrutiny over the value of new medicines where there is currently no existing treatment in Croatia for comparative purposes. This recognizes the appreciable number of new medicines in development, especially new biological medicines which are currently often priced at between US$100,000–US$400,000 (Euros 74,000–296,000) per patient per course or per year [2, 35, 36, 38, 60–62].

In conclusion, we have described the similarities and changes to the ordinance in Croatia for both new and established medicines including generics and biosimilars and the implications. In addition, the implications for savings through reordering the list of reference priced countries (ERP) as well as the subsequent implications for savings with IRP at ATC Level III to V versus ATC Level V alone. We hope the findings will be of interest to other European countries. In addition, demonstrate that European countries with smaller populations can be active with introducing a variety of measures when needed. This is in the best interests of all key stakeholder groups.

All authors approved the final version of the paper:

• LSB was the principal initiator of the paper, provided input regarding ongoing reforms in Croatia, was involved in the calculations of potential savings, wrote the first draft and critiqued subsequent drafts

• BBG critiqued the first draft based on his considerable experience in working with health authorities from different countries in analysing health reform policies. This first draft is used as a basis to develop the paper for submission and publication

• MB was heavily involved in the study design, provided input into ongoing reforms in Croatia, helped produce the first draft and critiqued subsequent drafts

• MS was principally involved with undertaking the calculations to ascertain potential savings from the different ordinances

H-YK and WB helped critique subsequent drafts based on their experiences

• TT was involved with the study design as well as critiqued the first and subsequent drafts

Competing interest: There are no conflicts of interest from any author. However, Ms Ljiljana Sović Brkićić is employed by CHIF, and Ms Martina Bogut is employed by the Ministry of Health Croatia.

This writing of this paper was in part supported by grants from the Karolinska Institutet, Sweden.

Provenance and peer review: Not commissioned; externally peer reviewed.

Ljiljana Sović Brkićić1, MPharm

Brian Godman2,3, BSc, PhD

Martina Bogut4, BSc

Miron Sršen5, MD

Hye-Young Kwon6,7, BPharm, MPH, PhD

Winnie de Bruyn8, BSc

Tonko Tabain9, MD

1Croatian Health Insurance Fund, 37 Branimirova, HR-10000 Zagreb, Croatia

2Division of Clinical Pharmacology, Karolinska Institute, Karolinska University Hospital Huddinge, SE-14186, Stockholm, Sweden

3Strathclyde Institute of Pharmacy and Biomedical Sciences, Strathclyde University, Glasgow, UK

4Ministry of Health, 200a Ksaver, HR-10000 Zagreb, Croatia

5Sygin istraživanje i razvoj Ltd, 3 Trg žrtava fašizma, HR-10000 Zagreb, Croatia

6Institute of Health and Environment, Seoul National University, Seoul, South Korea

7Department of Global Health and Population, Harvard School of Public Health, Boston, MA, USA

8Department of Pharmaceutical Sciences, Utrecht University, Utrecht, The Netherlands

9University of Zagreb, School of Medicine, Zagreb, Croatia

Authors are responsible for English language editing of this manuscript.

References

1. OECD. OECD, Health at a Glance 2011: OECD Indicators. Pharmaceutical expenditure OECD Publishing [homepage on the Internet]. [cited 2015 Apr 24]. Available from: http://dx.doi.org/10.1787/health_glance-2011-en

2. WHO. Access to new medicines in Europe: technical review of policy initiatives and opportunities for collaboration and research [homepage on the Internet]. [cited 2015 Apr 24]. Available from: http://www.euro.who.int/en/health-topics/Health-systems/medicines/publications2/2015/access-to-new-medicines-in-europe-technical-review-of-policy-initiatives-and-opportunities-for-collaboration-and-research

3. Godman B, Wettermark B, van Woerkom M, Fraeyman J, Alvarez-Madrazo S, Berg C, et al. Multiple policies to enhance prescribing efficiency for established medicines in Europe with a particular focus on demand-side measures: findings and future implications. Front Pharmacol. 2014;5:106.

4. Moon JC, Godman B, Petzold M, Alvarez-Madrazo S, Bennett K, Bishop I, et al. Different initiatives across Europe to enhance losartan utilisation post generics: impact and implications. Front Pharmacol. 2014;5:219.

5. Dylst P, Vulto A, Simoens S. Demand-side policies to encourage the use of generic medicines: an overview. Expert Rev Pharmacoecon Outcomes Res. 2013;13(1):59-72.

6. Dylst P, Simoens S. Does the market share of generic medicines influence the price level?: a European analysis. Pharmacoeconomics. 2011;29(10):875-82.

7. Godman B, Abuelkhair M, Vitry A, Abdu S, Bennie M, Bishop I, et al. Payers endorse generics to enhance prescribing efficiency; impact and future implications, a case history approach. Generics and Biosimilars Initiative Journal (GaBI Journal). 2012;1(2):69-83. doi:10.5639/gabij.2012.0102.017

8. Vogler S, Zimmermann N. How do regional sickness funds encourage more rational use of medicines, including the increase of generic uptake? A case study from Austria. Generics and Biosimilars Initiative Journal (GaBI Journal). 2013;2(2):65-75. doi:10.5639/gabij.2013.0202.027

9. Vogler S. The impact of pharmaceutical pricing and reimbursement policies on generics uptake: implementation of policy options on generics in 29 European countries–an overview. Generics and Biosimilars Initiative Journal (GaBI Journal). 2012;1(2):93-100. doi:10.5639/gabij.2012.0102.020

10. Leopold C, Vogler S, Mantel-Teeuwisse AK, de Joncheere K, Leufkens HG, Laing R. Differences in external price referencing in Europe: a descriptive overview. Health Policy. 2012;104(1):50-60.

11. World Health Organization. Espin J, Rovira J, Olry de Labry A. Working Paper 1: External reference pricing. WHO/HAI Project on medicine prices and availability. Review series on pharmaceutical pricing policies and interventions. May 2011 [homepage on the Internet]. [cited 2015 Apr 24]. Available from: http://www.haiweb.org/medicineprices/05062011/ERP%20final%20May2011.pdf

12. European Commission. European Economy. Carone G, Schwierz C, Xavie A. Cost-containment policies in public pharmaceutical spending in the EU. Economic Papers 461. September 2012 [homepage on the Internet]. [cited 2015 Apr 24]. Available from: http://ec.europa.eu/economy_finance/publications/economic_paper/2012/pdf/ecp_461_en.pdf

13. Simoens S. A review of generic medicine pricing in Europe. Generics and Biosimilars Initiative Journal (GaBI Journal). 2012;1(1):8-12. doi:10.5639/gabij.2012.0101.004

14. Brkicic LS, Godman B, Voncina L, Sovic S, Relja M. Initiatives to improve prescribing efficiency for drugs to treat Parkinson’s disease in Croatia: influence and future directions. Expert Rev Pharmacoecon Outcomes Res. 2012;12(3):373-84.

15. Voncina L, Strizrep T. Croatia: 2009/2010 pharmaceutical pricing and reimbursement reform. Eurohealth. 2011;16(4):20-2.

16. Godman B, Bennie M, Baumgärtel C, Sović Brkićić L, Burkhardt T, Fürst J, et al. Essential to increase the use of generics in Europe to maintain comprehensive healthcare? Farmeconomia: Health Economics and Therapeutic Pathways. 2012;13(Suppl 3):5-20.

17. Vogler S, Habl C, Bogut M, Voncina L. Comparing pharmaceutical pricing and reimbursement policies in Croatia to the European Union Member States. Croat Med J. 2011;52(2):183-97.

18. Voncina L, Strizrep T, Godman B, Bennie M, Bishop I, Campbell S, et al. Influence of demand-side measures to enhance renin-angiotensin prescribing efficiency in Europe: implications for the future. Expert Rev Pharmacoecon Outcomes Res. 2011;11(4):469-79.

19. Ministry of Health. Ordinance establishing the criteria for wholesale pricing of medicinal products and the manner of reporting wholesale prices. Official Gazette 155/2009.

20. Ministry of Health. Ordinance amending the corrections of Ordinance establishing the criteria for wholesale pricing of medicinal products and the manner of reporting wholesale prices. Official Gazette 22/2010. 2010.

21. Ministry of Health Croatia. Ordinance establishing the criteria for wholesale pricing of medicinal products and the manner of reporting wholesale prices. Official Gazette 83/2013 [homepage on the Internet]. [cited 2015 Apr 24]. Available from: http://www.hzzo.hr/zdravstveni-sustav-rh/pravilnik-o-mjerilima-za-stavljanje-lijekova-na-osnovnu-i-dopunsku-listu

22. Ministry of Health Croatia. Ordinance establishing the criteria for the inclusion of medicinal products to the basic and supplementary Reimbursement Lists of the Croatian Health Insurance Fund. Official Gazette 83/2013 [homepage on the Internet]. [cited 2015 Apr 24]. Available from: http://narodne-novine.nn.hr/default.aspx

23. Ministry of Health. Ordinance establishing the criteria for wholesale pricing of medicinal products and the manner of reporting wholesale prices. Official Gazette 12/2014. 2014.

24. Ministry of Health. Ordinance establishing the criteria for wholesale pricing of medicinal products and the manner of reporting wholesale prices. Official Gazette 69/2014. 2014.

25. WHO Collaborating Centre for Drug Statistics Methodology. ATC / DDD index 2011. WHO, Oslo. 2013 [homepage on the Internet]. [cited 2015 Apr 24]. Available from: http://www.whocc.no/atc_ddd_index/

26. European Commission. European Commission Directive. Council Directive 89/105/EEC of 21 December 1988 relating to the transparency of measures regulating the pricing of medicinaI products for human use and their inclusion in the scope of national health insurance systems [homepage on the Internet]. [cited 2015 Apr 24]. Available from: http://ec.europa.eu/health/files/eudralex/vol-1/dir_1989_105/dir_1989_105_en.pdf

27. Croatian Health Insurance Fund. Supplementary Reimbursement List of the Croatian Health Insurance Fund. Official Gazette 9/2014.

28. Croatian Health Insurance Fund Basic Reimbursement List of the Croatian Health Insurance Fund. Official Gazette 9/2014.

29. Croatian Health Insurance Fund. Objavljene liste lijekova [homepage on the Internet]. [cited 2015 Apr 24]. Available from: http://www.hzzo.hr/zdravstveni-sustav-rh/trazilica-za-lijekove-s-vazecih-lista2014

30. Ministry of Health of the Republic of Croatia. National Healthcare Strategy 2012–2020 [homepage on the Internet]. [cited 2015 Apr 24]. Available from: http://www.zdravlje.hr/programi_i_projekti/nacionalne_strategije/nacionalna_strategija_zdravstva.

31. Džakula A, Pavić N, Lonćarek K, Sekelj-Kauzlarić K. Croatia: health systems review. Health Systems in Transition. 2014;16(3).

32. Godman B, Malmstrom RE, Diogene E, Jayathissa S, McTaggart S, Cars T, et al. Dabigatran – a continuing exemplar case history demonstrating the need for comprehensive models to optimize the utilization of new drugs. Front Pharmacol. 2014;5:109.

33. Putrik P, Ramiro S, Kvien TK, Sokka T, Pavlova M, Uhlig T, et al. Inequities in access to biologic and synthetic DMARDs across 46 European countries. Ann Rheum Dis. 2014;73(1):198-206.

34. Cohen D, Raftery J. Paying twice: questions over high cost of cystic fibrosis drug developed with charitable funding. BMJ. 2014;348:g1445.

35. Kmietowicz Z. NICE says drug for metastatic breast cancer is unaffordable for NHS. BMJ. 2014;348:g2888.

36. The price of drugs for chronic myeloid leukemia (CML) is a reflection of the unsustainable prices of cancer drugs: from the perspective of a large group of CML experts. Blood. 2013;121(22):4439-42.

37. Kantarjian HM, Fojo T, Mathisen M, Zwelling LA. Cancer drugs in the United States: Justum Pretium—the just price. J Clin Oncol. 2013;31(28):3600-4.

38. Cohen P, Felix A. Are payers treating orphan drugs differently? Journal of Market Access & Health Policy. 2014;2:23513.

39. Leopold C, Mantel-Teeuwisse AK, Seyfang L, Vogler S, de Joncheere K, Laing RO, et al. Impact of external price referencing on medicine prices – a price comparison among 14 European countries. South Med Rev. 2012;5(2):34-41.

40. Godman B, Campbell S, Suh HS, Finlayson A, Bennie M, Gustafsson L. Ongoing measures to enhance prescribing efficiency across Europe: implications for other countries. J Health Tech Assess. 2013;1:27-42.

41. Paris V, Belloni A. Value in pharmaceutical pricing. OECD Health Working Papers, No. 63: OECD Publishing; 2013. doi.org/10.1787/5k43 jc9v6knx-en

42. Cassel D, Ulrich V. Ex-factory prices in European pharmaceutical markets as reimbursement framework of the German Statutory Health Insurance – issues and problems of international reference pricing for innovative pharmaceuticals. 22 February 2011. [cited 2015 Apr 24]. Available from: http://www.google.co.uk/url?sa=t&rct=j&q=&esrc=s&source=web&cd=1&ved=0CDgQFjAA&url=http%3A%2F%2Fwww.vfa.de%2Fdownload%2Fexsum-cassel-ulrich.pdf&ei=NjwYVLm4\NdPmaKKKgsAJ&usg=AFQjCNG0icytL-w7KXQ_mWsYtHsWbDWVbw

43. European Commission. Ferrario A, Kanavos P. Managed entry agreements for pharmaceuticals: the European experience: LSE; April 2013 [homepage on the Internet]. [cited 2015 Apr 24]. Available from: http://ec.europa.eu/enterprise/sectors/healthcare/files/docs/mea_report_en.pdf

44. Vogler S, Zimmermann N, Habl C, Piessnegger J, Bucsics A. Discounts and rebates granted to public payers for medicines in European countries. South Med Review. 2012;5(1):38-46.

45. Böttiger Y, Laine K, Andersson ML, Korhonen T, Molin B, Ovesjö ML, et al. SFINX-a drug-drug interaction database designed for clinical decision support systems. Eur J Clin Pharmacol. 2009;65(6):627-33.

46. Sjoborg B, Backstrom T, Arvidsson LB, Andersen-Karlsson E, Blomberg LB, Eiermann B, et al. Design and implementation of a point-of-care computerized system for drug therapy in Stockholm metropolitan health region—Bridging the gap between knowledge and practice. Int J Med Inform. 2007;76(7):497-506.

47. Stausberg J, Hasford J. Drug-related admissions and hospital-acquired adverse drug events in Germany: a longitudinal analysis from 2003 to 2007 of ICD-10-coded routine data. BMC Health Serv Res. 2011;11:134.

48. Pirmohamed M, James S, Meakin S, Green C, Scott AK, Walley TJ, et al. Adverse drug reactions as cause of admission to hospital: prospective analysis of 18 820 patients. BMJ. 2004;329(7456):15-9.

49. Brvar M, Fokter N, Bunc M, Mozina M. The frequency of adverse drug reaction related admissions according to method of detection, admission urgency and medical department specialty. BMC Clin Pharmacol. 2009;9:8.

50. Rottenkolber D, Schmiedl S, Rottenkolber M, Farker K, Salje K, Mueller S, et al. Adverse drug reactions in Germany: direct costs of internal medicine hospitalizations. Pharmacoepidemiol Drug Saf. 2011;20(6):626-34.

51. Miller I, Ashton-Chess J, Fert V, et al. Market access challenges in the EU for high medical value diagnostic tests. Personalised Medicine. 2011;8(2):137-48.

52. Vogler S, Zimmermann N, Leopold C, de Joncheere K. Pharmaceutical policies in European countries in response to the global financial crisis. South Med Rev. 2011;4(2):69-79.

53. Cramer JA, Benedict A, Muszbek N, Keskinaslan A, Khan ZM. The significance of compliance and persistence in the treatment of diabetes, hypertension and dyslipidaemia: a review. Int J Clin Pract. 2008;62(1):76-87.

54. Godman B, Alvarez-Madrazo S, Acurcio F, Guerra Junior AA, Faridah Aryani MY, et al. Initiatives among authorities to improve the quality and efficiency of prescribing and the implications. J Pharma Care Health Sys. 2014;1(3):1-15.

55. Jelicic Kadic A, Zanic M, Skaricic N, Marusic A. Using the WHO essential medicines list to assess the appropriateness of insurance coverage decisions: a case study of the Croatian national medicine reimbursement list. PloS One. 2014;9(10):e111474.

56. Gustafsson LL, Wettermark B, Godman B, Andersen-Karlsson E, Bergman U, Hasselstrom J, et al. The ‘wise list’– a comprehensive concept to select, communicate and achieve adherence to recommendations of essential drugs in ambulatory care in Stockholm. Basic Clin Pharmacol Toxicol. 2011;108(4):224-33.

57. Björkhem-Bergman L, Andersén-Karlsson E, Laing R, Diogene E, Melien O, Jirlow M, et al. Interface management of pharmacotherapy. Joint hospital and primary care drug recommendations. Eur J Clin Pharmacol. 2013;69 Suppl 1:73-8.

58. Godman B, Wettermark B, Hoffmann M, Andersson K, Haycox A, Gustafsson LL. Multifaceted national and regional drug reforms and initiatives in ambulatory care in Sweden: global relevance. Expert Rev Pharmacoecon Outcomes Res. 2009;9(1):65-83.

59. Serbian Health Insurance Fund. Wise List translated into Serbian. 2014 [homepage on the Internet]. [cited 2015 Apr 24]. Available from: http://rfzo.rs/download/farmakopolitika/Mudra%20lista%201.%20deo.pdf

60. Hillner BE, Smith TJ. Efficacy does not necessarily translate to cost effectiveness: a case study in the challenges associated with 21st-century cancer drug pricing. J Clin Oncol. 2009;27(13):2111-3.

61. Evaluate Pharma. Surveying tomorrow’s BioPharma landscape. The NASDAQ Biotech index up close. June 2012 [homepage on the Internet]. [cited 2015 Apr 24]. Available from: http://info.evaluatepharma.com/rs/evaluatepharmaltd/images/EvaluatePharma_NBI_Up_Close_2012.pdf

62. EFPIA. Health & Growth – Working together for a healthy Europe. A vision towards a life sciences strategy for Europe. 2014 [homepage on the Internet]. [cited 2015 Apr 24]. Available from: http://www.efpia.eu/uploads/documents/EFPIA-health&growth_MANIFESTO_V11_pbp.pdf

|

Author for correspondence: Brian Godman, BSc, PhD; Division of Clinical Pharmacology, Karolinska Institute, Karolinska University Hospital Huddinge, SE-14186, Stockholm, Sweden |

Disclosure of Conflict of Interest Statement is available upon request.

Copyright © 2015 Pro Pharma Communications International

Permission granted to reproduce for personal and non-commercial use only. All other reproduction, copy or reprinting of all or part of any ‘Content’ found on this website is strictly prohibited without the prior consent of the publisher. Contact the publisher to obtain permission before redistributing.

Source URL: https://gabi-journal.net/pharmaceutical-pricing-in-croatia-a-comparison-of-ordinances-in-2013-versus-2009-and-their-potential-savings-to-provide-future-guidance.html

Copyright ©2025 GaBI Journal unless otherwise noted.