The implementation of generics in France

Published on 2015/04/21

Generics and Biosimilars Initiative Journal (GaBI Journal). 2015;4(3):136-40.

|

Abstract: |

Submitted: 7 April 2015; Revised: 22 May 2015; Accepted: 24 May 2015; Published online first: 8 June 2015

Introduction

The official pharmaceutical market for prescription products is worth around Euros 28 billion, and generic drugs represent Euros 6 billion, accounting for 22% of the market and around 70% of all substitution products registered to the Generics Repertory.

Definition of a generic drug

Within patent legislation, the term ‘generic drug’ refers to a copy of a listed brand-name drug, whose patent and patent term restoration have expired, making the drug publically usable by any drug manufacturer.

In France, the first legal definition of a generic drug was given by France’s National Office of Fair Trading (Commission de la Concurrence) on 21 May 1981:

‘a generic drug is defined as any copy of an original drug, whose production and marketing are made possible after the expiration of the original drug patent, hence becoming part of the public domain once the legal protection period comes to term. The term ‘generics’ includes drugs sold under a brand name or an invented name, as well as drugs sold under an internationally common or chemically-descriptive non-proprietary name, which must be accompanied by a brand or manufacturer name.’

It was subsequently necessary to define the content and quality of generic drugs more precisely. The order 96–345 of 24 April 1996 introduced the first technical legal definition of a generic drug [1], which corresponds to the European definition as cited in the minutes of the Executive Council of December 1986.

This definition was later used in 1998 in a judgment of the Court of Justice of the European Communities [2], highlighting the unique property of the qualitative and quantitative composition of active principles as well as of the bioequivalence between the original (brand-name) drug and the generic drug. This same definition was further modified in 2004, following a ruling of the Court of Justice of the European Communities [3], this time highlighting the bioequivalence criterion requirement.

In 2005, another legal ruling [4] permitted any drug containing the same active fraction as the brand-name drug (from a therapeutic standpoint) to benefit from a shortened registration procedure. The excipient can, on the other hand, be a different salt, isomer or ester. By focusing on therapeutic effect rather than on molecular structure, the notion of a generic drug became closer to the notion of therapeutic equivalence; that is, with the same qualitative and quantitative effects. The technical rationale behind generic drugs now focused on in vivo results for quality assessment rather than on galenic form for oral administration. On the basis of these legal rulings and the above logic, the Directive 2004/27/CE adopted the extensive definition of a ‘generic drug’, hence, replacing the vague term ‘similar drug’ [5].

This definition is due to be incorporated into the Public Health Code in the section L.5121–1,5°a) [6]. Within this framework, the sanitary authorities will require additional and sufficient proof of the safety and efficacy of a generic drug if its active principle is not identical in pharmaceutical or salt form to the brand-name drug. In France, a Repertory of Generic Groups [7] has been established to allow for easy identification of generics as substitutes to brand-name drugs.

The 1999 Health Insurance Funding Act introduced the notion of right of substitution for pharmacists, as long as the prescriber has not excluded this possibility. In 2008, the prescription of International Nonproprietary Name (INN) drugs became mandatory for all branded pharmaceutical products [8].

A country reluctant to switch to generics

Compared with other high-income countries, e.g. Germany, the UK and the US, France is lagging behind in its introduction of generics to the pharmaceutical market. The first mention of the term ‘generic’ was in 1995 in the Prime Minister’s Health Plan to reduce public health spending:

‘The generic version of a reference branded product is defined as having the same qualitative and quantitative composition in terms of active principles, the same pharmaceutical form and whose bioequivalence with the reference product is demonstrated by relevant studies of bioavailability.’

At that time, pharmaceutical manufacturers considered generic drugs a potential threat to their products and doubted their economic benefit, given the high cost of drugs at the time; the medical profession, with lack of knowledge of health economics, were dismissive of pharmaceutical manufacturers, who they perceived to be rushing into the market to duplicate and exploit the discoveries of others.

Physicians believed that they were still in control of treatment, with the autonomy to choose the molecule, brand and manufacturer of a drug. Pharmacists were strongly opposed to the idea of cheaper drugs, because of the difficulty of stocking larger quantities of drugs, even if greater quantities should be sold, because they would be less profitable. The public, in the meantime, were completely unaware of developments in this area and what was at stake.

The French generics pharmaceutical company Laboratoire Français de Produits Génériques was established in the 1980s but was boycotted by pharmacist unions and by its parent pharmaceutical company Clin-Midy. This boycott of generics was condemned in July 1981 by the French Ministers of Finance, René Monory and after Jacques Delors.

In reality, generic drugs were available before 1995, and were copies of drugs whose patents had expired and which therefore benefited from a simplified registration procedure. Often, those were copies of the original molecule manufactured by the same brand as the original drug once the patent had expired, making them indistinguishable from their brand-name counterparts to both the public and health professionals. These generics were promoted among prescribers and sold under the same brand name by new pharmaceutical companies specially created to sell these generics (at a price lower, about 20%), and not well recognized by major companies at prices slightly lower than the brand-name drug prices. Biogalenique Laboratory was one of these new companies and was controlled secretly by Pierre Fabre Laboratories.

The history of generic drugs in France

Generic drugs first gained real recognition with the announcement of the Retirement and Social Security plan by Prime Minister Alain Juppé on 15 November 1995.

In 1994, Mr Jean Marmot, magistrate at the audit office, became the first President of the Economic Committee for Healthcare Products, the interdepartmental government body in charge of regulating the prices of reimbursable drugs. A fervent supporter of generics, he inspired the provisions of Prime Minister Juppé’s plan before they were even set out, and drew up and signed agreements with pharmaceutical manufacturers to sell their products at 70% of the cost of brand-name drugs, using the INN in exchange for more favourable conditions for accessing the pharmaceutical market for their innovative products. This gave pharmaceutical manufacturers the freedom to fix the prices of their own new products.

This type of agreement ultimately benefitted the public accounts, but also became popular among innovative pharmaceutical manufacturers, without perturbing their brand image, who initiated acquisitions, began to develop a range of generic drugs, or both, often through affiliated companies dedicated to this task. In 1995, for example, Rhône-Poulenc Rorer acquired Biogalenique, later renamed ‘Rhône-Poulenc Génériques’. Sanofi also established a generics department, which subsequently became Ratiopharm. Although the price-agreement policy was instrumental to the emergence of generics, a fundamental element of the market was missing: demand.

The second act was in 1999, when the Chairman of the pharmaceutical unions federation of France (Fédération des Syndicats Pharmaceutiques de France), Mr Bernard Capdeville began campaigning for the ‘right of substitution’. Despite opposition from physicians, and, especially, general practitioners, he lobbied the medical profession and public authorities to support the principle of equal profit margins between generic and brand-name drugs.

Approval of this new measure ensured by all pharmacist unions reduced the potential economic gain of generics for public authorities. The authorities subsequently backed down admitting that they could not move forward without pharmacist support, and agreed to relax the system of ‘smoothed decreasing profit margin’ established in 1990.

In order to calm the strong medical opposition, public authorities restricted the ‘right of substitution’ to ‘generics groups’; that is, the ensemble composed of a brand-name drug and its generics registered by the Drug Agency. Then, all the generics groups were brought under the umbrella of the ‘Generics Repertory’, a unique reference directory used by western countries, which contains more than 1,000 generics groups relating to 370 molecules [9]. In France alone, a generic drug cannot be substituted unless it has been registered with the Generics Repertory. Therefore, even today, high-volume drugs such as paracetamol or aspirin whose generics have existed for a long time, are excluded from the substitution system under the pretext that a unique identifiable brand-name drug able to constitute a generic drug group no longer exists.

At this time, the strategic choice of betting on pharmacists paid off slowly but surely. The generics market took off but with rates of substitution well under the expected 35%. Physicians and patients still remained reluctant to switch to generics, and exercised their right to access original brand-name drugs, with no penalty.

The third act was in June 2002, when the newly constituted government, with Professor Jean-François Mattei as the new Minister of Health, gave in to the demands of the three main physicians unions (MG France, Syndicats des Médecins Libéraux (SML) and Confédération des Syndicats Médicaux de France (CSMF)) to increase the cost of a general practitioner’s medical consultation at Euros 20. Underpinning this was a focus on generics, with physicians requested to stop their active counter propaganda against generics. At the same time, the public authorities significantly increased the discounts agreed by manufacturers to pharmacists and further decreased the smoothed decreasing profit margin. Now it became more profitable for a pharmacist to sell a generic drug than a brand-name drug. The market finally took off and the expected substitution target of 35% was attained.

The fourth act was when the generic drug system was transferred from the government to the Health Insurance System in 2010 introducing innovative new changes in relation to generic drugs. First, an agreement was reached between the French National Health Insurance Agency and pharmacists to increase the substitution target to 80% for 20 of most prescribed molecules on the market, with advantages for pharmacists.

The second change, and one that had the biggest impact of all, was initially implemented by the Regional Health Insurance Agency of the ‘Alpes Maritimes’ region, during spring 2011. Only patients accepting substitution drugs (generics) were permitted to receive an advance on costs. The idea of a ‘third-party payer in exchange for generics’ was the first time that patients considering using generic drugs could benefit financially. This was also effective at the treasury level for accounting reasons, because if the patients wanted the brand-name drug they had to pay it and were reimbursed only three to four weeks after.

This initiative was quickly rolled out to other territories, covering all of France by June 2012: at this point, the plan included all pharmacists, all medical prescriptions, all medical products, and nearly all patients. The possibility of a ‘non-substitutable’ mention for the prescriber remained open but it had to be handwritten and was only applicable per product and not for the entire prescription.

The fifth act was between 2009 and 2012, when two important developments took place. First the French National Health Insurance Agency intervened to fix the depletion of the drug Repertory resulting from the expiration of drug patents for the most commonly used molecules, making them fall in the public domain.

A shift in prescribing was then observed to-wards products of the same therapeutic class as brand-name drugs but which were not generics. This move away from brand-name drugs, which blocked the substitution system, was a result of the weak promotion of generics in favour of competitors’ ‘non-repertory’ products still patented and actively promoted. This observation led to the decision to include prescribing in the scope of the Generics Repertory in the new performance-related pay system established in 2009 as part of the French general practitioner’s performance-related pay contract, and was presented to physicians willing to sign up.

The French National Health Insurance Agency requested general practitioners to meet certain objectives (related to increased prescribing of substitution products for certain classes of commonly used drugs), which, if achieved, would be paid in the form of bonuses. This plan was a great success and was implemented with reinforced objectives, to be later added to the medical agreement under the name ‘Contract for Improvement of Individual Practices’. It was signed by 75,000 physicians and anticipated to make each physician earn up to Euros 5,000 more per year, see Figure 1.

A similar performance-related pay system was implemented for pharmacists through a conventional agreement on 4 May 2012. It included an explicit list of about 30 generic drug groups and set target substitution rates, which varied according to the molecule, and depended on their nature, time spent on the market, and mean age of the patient. Target rates varied between 42% for osteoporosis drugs and 95% for pravastatin. At this stage, the projected goal was a global rate of substitution of 85% by the end of 2012.

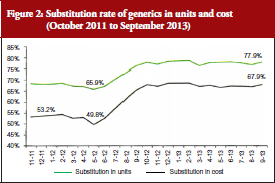

Coupled with the reinforcement of the ‘third-party payer in exchange for generics’ system mentioned above, this performance-related pay system was successful; reaching a 12% higher substitution from June 2012, see Figure 2. The rates stabilized at around 70% in cost and around 80% in units, with no observed decrease.

Finally, the sixth act was a ruling on the Bertrand Law (from 29 December 2011), which came into effect on 1 January 2015: the generalization of INN prescriptions recommended by the World Health Organization. This provision further promoted the substitution movement, as long as prescribers possessed the correct prescription softwares, of which 39 were certified by the French National Authority for Health.

Historical lessons learned

The establishment and acceptance of generic drugs in France has been a protracted and cumbersome process compared with other countries, which have had a better take-up of generic drugs.

In countries with multiple insurance systems, either private (the US) or public (Germany and The Netherlands), the initiative to implement generics has always come from the insurers, with efforts primarily focused on convincing patients to accept prescribed generic drugs. The simplest system, known as the ‘reference price’ system, was introduced in Germany and The Netherlands in the late 1980s. This system took the price of generic drugs as the basis for reimbursing the cost of drugs, regardless of whether the patient chose a brand-name drug or the generic drug. A harsher version of this same system was implemented in the US by Managed Care organizations, and involved only reimbursing the cost of generic drugs listed in the formulary for reimbursement; a patient wishing to purchase a brand-name drug would be personally liable for the cost.

In one way or another, the policies that have succeeded in encouraging take-up of generic drugs by the patients are based on demand (prompted or forced), which have led to an immediate acceptance of a generics offer, later regulated by public authorities for clarification and organization purposes.

In France, with its centrally administered economy and mistrust of the market’s inner workings, a policy of ‘offer’ was initially devised, with a subsequent re-worked policy of ‘demand’ only when the former failed to produce results. The government had initially wanted to protect the patient, and, after the failure of the policy between the government and pharmaceutical manufacturers, the French Health Insurance Agency intervened to stimulate demand by offering financial incentives for health professionals and patients. This two-step process would have been fine, had it not taken 10 years to happen.

One of the reasons for this reverse logic is the persistence of an administrative system to fix the price of generics. Public authorities have precluded any system of competition, including between manufacturers, by fixing administrative prices for generic drugs (same prices for all generics belonging to the same group). In other countries, it is rather the competition between manufacturers that is responsible for price reductions, often greater than those obtained through the French public regulation system. This competition also leads to the emergence of global leaders and, in turn, to the delocalization of production sites in low cost locations.

Opening the generics market up to competition is still being debated today, and it has been loudly suggested that public authorities open the call for tender to entrust some pharmaceuticals with the entire market, e.g. statins, proton pump inhibitors, giving the best guarantees, as was the case in Germany and in The Netherlands, reducing prices drastically. The French Health Insurance fund prefers a system of well-advised buyers by making sure that public funds and pharmacists split the profits, a model similar to the UK system.

Ironically, the story of generics in itself demonstrates the paradox that financial incentives do produce results when the main health actors have little interest for health economic questions. Health professionals only agreed to the objective of efficacy because they were offered direct profits. Also patients, forced to switch to generics, responded positively to the ‘third-party payer in exchange for generics’ plan beyond expectations. Generics have therefore highlighted a contradiction in the French healthcare system, displaying an obvious aversion for economic issues while resorting to financial incentives to stimulate the generics market.

The poor handling of the generics issue, particularly in the context of drug dispensing, has been evident through Internet blogs and social networks, where the public has vented its frustration, often with a misinformed view of the subject, and with access to partial information. Such frustration is easily understandable in view of the obvious disregard for the patient’s best interests during implementation of the first generics policy. During that time, health authorities were focused on imposing generics on the physician community against their will via pharmacist arm-twisting, and patients were feeling left out in terms of financial benefits.

Health is priceless, but has its costs. The proclamation of experts that cheaper treatments are as efficient as costly treatments are not ringing true with French consumers, as they are used to intuitively factoring in price as a quality indicator. The questioning of pharmaceutical quality and similarity of generics has become even more widespread following the publication of a heated report from the Academy of Medicine [10]. Its high-level political, scientific and suspicious economic discourse has left the public with mixed feelings about generics.

Will biosimilars follow the success of generics?

The future of generics in France and in developed countries is rather predictable. Generic drugs are about to become everyday drugs prescribed for almost all common diseases in all therapeutic domains. In most cases of common diseases, except for the thyroid disease, the current prescribed drugs are generics, see Table 1.

This situation is likely to last, at least for the next decade or two, until an important pharmaceutical innovation comes along to change the market share ranking of commonly sold molecules in these therapeutic areas. On the other hand, the flood of new generics is bound to dry up as a result of fewer innovations for commonly sold products in the past 20 years (duration of a patent). Therefore, the generics market seems stable for now and the model may spread to other countries where prices will yield under the pressure of payers either through administrative channels (as in western countries) or through competition.

Pharmaceutical research has long shifted from the big domains of traditional common diseases to the exploration of diseases such as cancers, autoimmune diseases and genetic diseases. It is here that true theoretical breakthroughs are needed, with new technological paradigms, e.g. targeted therapy, gene therapy, cell therapy, and that pharmaceutical manufacturers are not afraid to invest money in these. This active investment in innovative technologies is what shapes the market today. Among the top 20 products in the pharmaceutical market, two-thirds are recent high biotechnology products: monoclonal antibodies, antitumour necrosis factor, recombinant insulin, haematopoietic growth factors, granulocyte colony-stimulating factor, and erythropoietins, in addition to targeted anticancer therapies and, more recently, antiviruses.

The question is will this new costly innovation wave, which started in the 1980s and developed over a 20-year period, generate a new wave of generics when patents start to expire? No, it will not. These big molecules, copies of recombinant proteins with lost patents, are difficult to produce industrially from genetically modified live cells and cannot be compared with generics; either legally, medically or economically. Production conditions are such that, in 2005, the European Medicines Agency requested clinical efficacy trials to be conducted for ‘biosimilar’ drugs [11], contrary to generics, in which only a proof of pharmaceutical bioequivalence is necessary. European regulations state that, under certain circumstances, if the reference biological drug is prescribed in several indications, the biosimilar can be used for these same indications, even if it has been tested for only one of them. These products will create a new market for biosimilars, characterized by very different operational rules and by highly specialized high-tech pharmaceuticals. Biosimilars will not be generics, but their market may, in the coming years, play a role similar to the generics market.

Finally, the subject of small complex chemical molecules has been discussed internationally and also at the European level since 2009. These molecules are difficult to manufacture and, even though they may fit the definition of generic drugs, the generics market approach cannot be applied here. These molecules are commonly referred to as non-biological complex drugs [12]. As with biosimilar drugs, these few molecules are quite complex with iron sucrose (not registered in the Generics Repertory) being the main representative member of this class of active principles [13]. They are complex because the structure of these molecules depends partly on manufacturing conditions and is, therefore, specific to each manufacturer. This type of molecule could benefit from tailored registration regulations with appropriate risk-management plans.

Conclusion

With sustained financial means from society and from the French Health Insurance Agency, the savings generated by the use of generic drugs are ensuring better and cheaper access to costly therapeutic innovations for patients. The implementation of generics must hence be perceived as a sign of therapeutic progress and not as an obstacle. It is, therefore, paramount that health professionals unconditionally support all policies in favour of generics from now on, particularly because physicians are the main conduits of information for patients.

Acknowledgement

The authors wish to thank the English editing support provided by Ms Maysoon Delahunty, GaBI Journal Editor, for this manuscript.

Competing interest: None.

Provenance and peer review: Not commissioned; externally peer reviewed.

Co-author

Jessica Nasica-Labouze, PhD, Laboratoire de Biochimie Théorique, IBPC, CNRS, Paris, France & International School for Advanced Studies (SISSA), Trieste, Italy

References

1. Journal Officiel de la République Française du 25 avril 1996 N° 98 page 6311-l’article 23 établit une définition des médicaments génériques et dispose que la publicité qui leur est relative mentionne leur nature de spécialités génériques.

2. CJCE, 3 décembre 1998, AFF, C368-396, Generics et al.

3. CJCE, 29 avril 2004, AFF, C-106/01, Novartis.

4. CJCE, 20 janvier 2005, AFF, C-74/03, Smithkline Beecham.

5. Médicaments génériques et droit de la concurrence, Evgéniya Petrova. Thèse de doctorat en droit des affaires- présentée et soutenue publiquement le 17 juillet 2009 – Université Jean Moulin Lyon 3 – école doctorale de droit. Available from: http://www.acadpharm.org/dos_public/RAPPORT_GEnEriques_VF_2012.12.21.pdf

6. Journal Officiel de la République Française du 27 février 2007 – Loi 2007-248 du 26 février 2007 portant diverses dispositions d’adaptation au droit communautaire dans le domaine du médicament.

7. Article L5121-10 et R.5121-8 du Code de la Santé Publique. Available from:

http://ansm.sante.fr/var/ansm_site/storage/original/application/52e5390a6f9e8580d73bca744a516503.pdf

8. Journal Officiel de la République Française du 26 décembre 2001- Loi n° 2001-1246 du 21 décembre 2001, art. 19-1 (article L5125-23 du Code de Santé Publique).

9. Agence nationale de sécurité du médicament et des produits de santé. Répertoire des Groupes Génériques. 10 avril 2013.

10. Menkes JC. Place des génériques dans la prescription. Académie nationale de Medicine. février 2012.

11. European Medicines Agency. Guideline on similar biological medicinal products containing biotechnology-derived proteins as active substance: non-clinical and clinical issues. EMEA/CHMP/BMWP/42832/2005. EMEA. 2006 [homepage on the Internet]. [cited 2015 May 22]. Available from: http://www.ema.europa.eu/docs/en_GB/document_library/Scientific_guideline/2009/09/WC500003920.pdf

12. Schellekens H, Klinger E, Mühlebach S, Brin JF, Storm G, Crommelin DJ. The therapeutic equivalence of complex drugs. Regul Toxicol Pharmacol. 2011;59(1):176-83.

13. Rottembourg J, Kadri A, Leonard E, Dansaert A, Lafuma A. Do two intravenous iron sucrose preparations have the same efficacy? Nephrol Dial Transplant. 2011;26(10):3262-7.

|

Author for correspondence: Professor Jacques Rottembourg, MD, Department of Nephrology, Hôpital de la Pitié, 83 Boulevard de l’Hôpital, FR-75013 Paris, France |

Disclosure of Conflict of Interest Statement is available upon request.

Copyright © 2015 Pro Pharma Communications International

Permission granted to reproduce for personal and non-commercial use only. All other reproduction, copy or reprinting of all or part of any ‘Content’ found on this website is strictly prohibited without the prior consent of the publisher. Contact the publisher to obtain permission before redistributing.